Daniel Lacalle is Chief Economist at Tressis SV, has a PhD in Economics and is author of “Escape from the Central Bank Trap”, “Life In The Financial Markets” and “The Energy World Is Flat” (Wiley)

Images courtesy @IEB

Daniel Lacalle is Chief Economist at Tressis SV, has a PhD in Economics and is author of “Escape from the Central Bank Trap”, “Life In The Financial Markets” and “The Energy World Is Flat” (Wiley)

Images courtesy @IEB

I believe this is a truly excellent article explaining expansionary monetary policies and outlining the possibilities of unwinding quantitative easing programs. Eighteen global leading economists share their opinions.

Please read all the comments at Focus Economics here.

My part:

“The Federal Reserve is already seriously behind the curve. Reducing the balance sheet by $600bn after a $4.7 trillion stimulus and delaying rate hikes simply make the problem more difficult to solve as we approach a change of cycle and the central bank finds itself with fewer tools. The Federal Reserve should take advantage of the unprecedented demand for USD and the fact that macro drivers and corporate profits are improving to accelerate its unwinding of the stimulus. However, it seems comfortable ignoring the risks of perpetuating bubbles in financial assets. By being too focused on financial markets it becomes what I call in my book “Escape from the Central Bank Trap” a “pyromaniac firefighter” that creates a massive bubble and presents itself as the solution when it bursts.

The Federal Reserve could be raising rates and unwinding its balance sheet by $50-100bn every month now that demand for bonds and equities remains solid and the employment, inflation and growth data is improving, while earnings estimates are increasing. There would be more than ample secondary market demand for a solid sterilization program.

The ECB is caught between a rock and a hard place. It is on its way to reaching a balance sheet size of more tan 25% of GDP of the Eurozone and inflation expectations are falling, unemployment and slack are still high, proving that the problem of the Eurozone was never of liquidity and low rates. When the ECB QE started, excess liquidity was c€185bn and today it is close to €1.3 trillion. In the process, highly indebted and deficit-spending countries saved billions in interest payments,… but their imbalances remain and they have spent those savings and more, making it almost impossible for the ECB to taper and raise rates because high-deficit countries would be unable to assume it. But at the same time, the overcapacity of the economy is perpetuated and many countries are calling for further spending increases and widening deficits. The ECB, therefore, needs to give a stronger message to governments so that they accelerate reforms to reduce excess spending and improve growth, lower taxes. If the ECB starts a sterilization program and manages long-term rates adequately, it could successfully promote structural reforms, help spur growth and use that massive excess liquidity to keep bond yields low while governments improve their fiscal position. This would reduce the perverse incentives that some may have to increase imbalances just because QE is there. Furthermore, as the crisis is way behind us, the ECB’s purchases would be easily offset by real investor demand, as fundamentals improve. There is still time before Europe enters a dangerous “Japanization” process.”

Courtesy Focus Economics. Follow @FocusEconomics

Daniel Lacalle is Chief Economist at Tressis SV, has a PhD in Economics and is author of “Escape from the Central Bank Trap”, “Life In The Financial Markets” and “The Energy World Is Flat” (Wiley)

See more at: https://www.dlacalle.com/what-does-dr-copper-tell-us-about-global-growth/#sthash.AmZP9FEL.dpuf

Weakness in Copper persists, and it shows the risks to optimistic global growth and inflation expectations.

This weakness is down to a number of reasons:

Copper is the commodity that is most linked to industrial production. Copper price is a good indicator of the global economy as fluctuations in price are usually determined by industrial demand. Given that Chinese demand represents approximately 50% of global copper demand, the slowdown of its economy has a big impact on the price.

Additionally, many of the low-quality loans in China use copper as collateral, up to 30% according to HSBC, as it is an indicator of industrial activity and closely linked to Chinese growth. When the market begins to question the debt repayment capacity of many Chinese companies, margin calls are triggered and copper falls with it.

It is a double impact: Financial and demand-led. What was supposed to be a good hedge is actually a double risk on the economic slowdown.

Lower demand growth, persistent overcapacity.

The estimated surplus of refined copper was recently revised up, despite some moderation in production.

According to Platt’s:

The global refined copper market saw a surplus of around 165,000 mt in the first quarter of 2017, according to preliminary data released Tuesday by the International Copper Study Group.

“This is mainly due to [a] decline in Chinese apparent demand,” analysts with the Lisbon-based research firm said in a report. China currently represents 47% of the world copper refined usage.

Factoring in changes to private, unreported copper stocks in China, the first-quarter surplus rose to about 310,000 mt, it said.

Chile accounts for c34% of the world’s copper production, approximately 19% of the revenues for the country. USA is the fourth largest copper producer in the world, after Chile, Peru and China, and Australia is fifth. All these countries are producing at peak levels, and a small decrease of 3.5% year-on-year has failed to address the surplus.

In terms of demand, China accounts for c50%, followed by Europe 17%, other Asia 15%, U.S. c8%, Japan 5%. The rest are minor consumers.

Risks to demand estimates for refined copper in China, despite improved European indicators, mean that overcapacity increases. Current demand growth estimates are factoring a stronger US economy and a large infrastructure plan that is curtrently at risk of being severely delayed.

Refined copper overcapacity has remained since 2014, and calls for a “next year market balance” have been incorrect. China has seen its stockpiles of copper grow and it is looking to start exporting, just as supply continues to exceed demand.

Structural overcapacity and downward revisions of demand growth are the main drivers of the weakness in copper prices.

In summary, what Dr Copper is telling us loud and clear is that the infamous “reflation theme” that mainstream analysts have defended is simply incorrect, and that excessively optimistic expectations of global growth and inflation have to be revised down.

Daniel Lacalle is Chief Economist at Tressis SV, has a PhD in Economics and is author of “Escape from the Central Bank Trap”, “Life In The Financial Markets” and “The Energy World Is Flat” (Wiley)

@dlacalle_IA

Picture courtesy of Bloomberg

– See more at: https://www.dlacalle.com/video-buy-us-dollar-assets-opportunities-and-risks-after-the-fed-rate-hike/#sthash.Of4w0L2y.dpuf

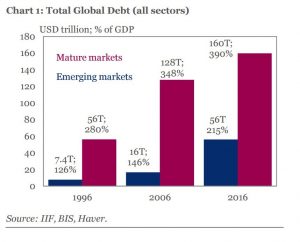

Global debt has soared to 325% of world GDP, led by increases in public debt precisely from those countries that have not implemented any kind of austerity. Public debt, in particular, has doubled in the US and China since 2006, and rose 50% in Japan and the Eurozone.

(Graph courtesy Daily Telegraph)

It is curious, or a symptom of partisan demagoguery, that the same ones that demand more stimulus and deficit spending- more debt -, raise their concerns because debt rises. It is almost a joke that mainstream proposes more white elephants and more public spending, only to fail.

“Spend to grow” has resulted in “spend to multiply debt”.

The mirage of public spending multipliers has proved-again-to be inexistent. The increase in public debt from the US to China and in the emerging countries that decided to “spend to grow” far exceeds real GDP growth since 2006 (read here). The real conclusion is that multipliers are very low or negative in open and indebted economies, precisely because they come from previous excesses created by those same “stimulus” plans.

The “expansion policies” proposed by the new inflationists have been an incorrect decision in the face of evident debt saturation. Why? Because what we are experiencing is a shock of oversupply, which leads to price declines, not a deficiency of aggregate demand. What we live is an environment of excess capacity after a decade of aggressive expansion in the face of growth expectations that did not come true. Overcapacity is evident in all major economies (read this Bloomberg post), as shown in this chart.

In fact, it has been shown that in an open economy with globalized trade and flexible exchange rates, the effectiveness of fiscal expansion is extremely limited (read this report).

Is public investment necessary? Like the private one, only if – as Lord Keynes said – it has a real economic return (read “What Keynes Really Said About Deficit Spending” ) and an obvious need. If not, it is not an investment, only spending to “sustain GDP” … And we know that wasteful spending leaves behind more debt and reduces potential growth. Overcapacity has moved from developed countries (22%) to emerging ones (Brazil about 30%) and China (more than 38%).

The fallacy of the multiplier of public spending has been demonstrated in many studies (read).

The history of more than 44 countries shows that the multiplier effect is very poor in open economies, and negative in highly indebted ones.

The study of Ilzetzki et all, ” How Big (Small?) Are Fiscal Multipliers? “analyzes the history of the cumulative impact of public spending in 44 countries, showing the very low effectiveness of fiscal stimuli.

Even if we accepted positive fiscal multipliers, the empirical evidence of the last fifteen years shows a range that, when positive, moves barely between 0.5 and 1 at most … and in most countries has been negative (“Has the IMF proved multipliers are really large?“).

Indeed, even studies analyzing a positive effect of public expenditure (read) warn that advanced and indebted economies are on the verge of their fiscal limit and their estimates lose credibility (“the effects of the monetary and fiscal policy instruments become unpredictable, and specifically, fiscal policy announcements lose credibility “).

The real conclusion – that the multipliers are very low or negative in open and indebted economies – is what is highlighted in the study by Corsetti et all (2012) ” What Determines Government Spending Multipliers? : “Fiscal multipliers are negative in times of weakness in public finances”.

In addition, massive public spending has a historically negative and dangerous impact on risk premiums, as shown by Bi, H. (2012): ” Sovereign Default, Risk Premia, Fiscal Limits, and Fiscal Policy“.

The current increase in debt has been fueled by the massive drop in interest rates, increased liquidity and wrongly-called expansionary plans, which generate excess debt and high refinancing needs that subsequently lead to a crisis, higher taxes, and subsequent larger budget cuts.

The perverse incentive to spend the money of others to cover the excesses of the past generates an increasing allocation of capital to low productivity sectors and the current expenditure is financed with higher taxes to the middle classes and high productivity industries. The so-called expansionary policies turn into a huge transfer of wealth from the productive sectors to the unproductive ones and, as it could not be otherwise, the potential growth is closed and the goals are broken.

The so-called expansionary policies turn into a huge transfer of wealth from the productive sectors to the unproductive ones, impacting potential growth and weakening the economy.

This endangers the ability to finance the economy and ends in a crisis. That is why debt shocks occur in countries, not because of their high indebtedness alone, but due to the continued deterioration of their public accounts.

One cannot criticize the rise in public debt and demand more deficits. It is like criticizing drunkenness and proposing to cure it with vodka

Very few countries -Germany, Ireland, Estonia, not many more- are implementing real measures to reduce public debt in absolute terms. Almost everyone, moderately or aggressively, makes plans assuming science fiction revenues calculated by people who know that the average error in estimates of future revenues is shameful and, of course, without contingency plans. We must think about the risk of debt shock when we meet in 2018 to 2020 with global repayments to refinance of more than one trillion dollars annually.

We must think about the risk of debt shocks when we face between 2018 and 2020 global refinancing needs of more than one trillion dollars annually. If countries decide to tackle this rise in debt spending a lot more, we will enter that crisis with much less capacity for reaction.

To think that excess debt is solved by borrowing more is like thinking that dancing in a circle will attract rain

Debt is not a right, nor an asset for a country. It is a dangerous liability. In the face of the risk of global debt accumulation, the policy should not be to join everyone to the edge of the cliff but to go in the opposite direction.

To think that the excess debt is solved by borrowing more is like thinking that dancing in a circle will attract rain.

Daniel Lacalle has a PhD in Economics and is author of “Escape from the Central Bank Trap”, “Life In The Financial Markets” and “The Energy World Is Flat” (Wiley)

@dlacalle_IA

Picture courtesy of Google