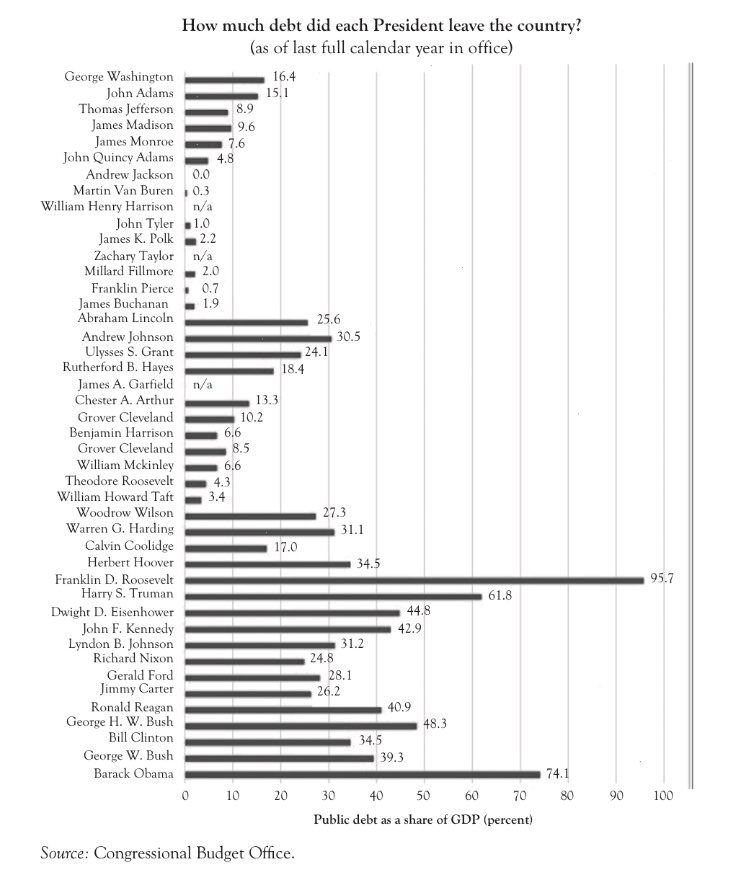

Very few people pay attention to the debt ceiling risks, and for a reason. The debt ceiling has been raised 74 times since March 1962. I commented it in the BBC as far as 2013 (here). It is, therefore, logical that investors and citizens believe that it will be raised yet again in September. Continue reading The Debt Ceiling… And Why It Matters

Very few people pay attention to the debt ceiling risks, and for a reason. The debt ceiling has been raised 74 times since March 1962. I commented it in the BBC as far as 2013 (here). It is, therefore, logical that investors and citizens believe that it will be raised yet again in September. Continue reading The Debt Ceiling… And Why It Matters

All posts by Daniel Lacalle

Video: Reign In Europe’s Pyromaniac Firefighters | Interview @ Real Vision

Central banks are behaving like pyromaniac firefighters, presenting themselves as the solution to the crises their policies create.

In this interview at Real Vision, we discuss this issue.

Daniel Lacalle is Chief Economist at Tressis SV, has a PhD in Economics and is author of “Escape from the Central Bank Trap”, “Life In The Financial Markets” and “The Energy World Is Flat” (Wiley)

Follow Real Vision at @Realvision

Are Central Banks Nationalising the Economy?

The FT recently run an article that states that “leading central banks now own a fifth of their governments’ total debt”.

The FT recently run an article that states that “leading central banks now own a fifth of their governments’ total debt”.

The figures are staggering. Without any recession or crisis, major central banks are purchasing more than $200bn a month in government and private debt, led by the ECB and the Bank of Japan.

Continue reading Are Central Banks Nationalising the Economy?

Is The Euro Crisis Really Over?

This week we have read that Brussels has certified “the end of the crisis”. In an uncomfortably triumphant statement, the group welcomed the fact that Europe had emerged from the crisis and returned to growth “thanks to the decisive action of the European Union”.

This week we have read that Brussels has certified “the end of the crisis”. In an uncomfortably triumphant statement, the group welcomed the fact that Europe had emerged from the crisis and returned to growth “thanks to the decisive action of the European Union”.