My comment on CNBC on the 24th Sept.

I will not go into aggressive and emotional debate that many use with Catalonia. I just wonder … If the fiscal benefit (balanza fiscal) is so large and the solvency of independent Catalonia is so obvious, why is it not recognized by rating agencies and investors?

The Catalan bond has junk status , according to Standard & Poor’s. You may think it is “because Spain robs them”. But no rating agency, either Moody’s, S&P or Fitch, grants the slightest advantage to independence. None of them say something like “if Catalonia were to become independent they would be Investment Grade “. They say the opposite and clearly. Without the support of the central government the risk is higher.

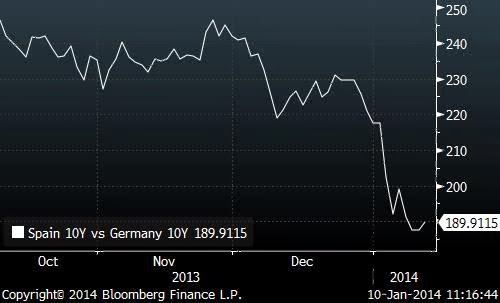

The Catalan 10 year bond has the widest premium to Germany of the EU after Greece. No other region or country has a higher financing cost. In fact, since secession messages began prior to the elections, the Catalan 2020 bond´s risk premium has risen by 100bps.

I’ll try to explain two concepts in the bond market that many do not take into account. A “credit event” and “underlying risk.” These are the arguments of independentists debunked:

“… What rating agencies say does not matter because they are influenced by the Spanish Government and have no credibility”

Suppose it was that way. That Moody’s, Standard & Poor’s, Fitch, Merkel, investment banks, Cameron and Hollande are all “kidnapped” by the Spanish central government, even though it has never been able to influence these entities in the past when they had negative views of Spain. Assume that those people and entities have vested interests but the separatists are all altruistic, even if it is at least childish. Just remember that the rating agencies have historically failed for being optimistic, not pessimistic, hence their mistakes in the crisis. If you think that agencies have no credibility in saying that independence is an increased risk, at least have very clear that they are being diplomatic.

“… But the Catalan debt is guaranteed by the Spanish State, and if we don´t want we will not pay it”.

Welcome to a “credit event”. Suppose a country owes all its debt to a single nation. With default, everyone will be happy and the country will finance itself like royalty, right? It is not like this. The risk is not reduced, it multiplies. Because reliability as a debtor is destroyed. Not only will refinancing be more expensive. It is more difficult to access markets. See the case of Ecuador, which defaulted and it took years to access the debt markets. When it finally came to issue bonds, it was for a very small amount at 7.95% for ten years in dollars. Today it is financed at 10.5%. And it is an oil rich country.

“… But the new Catalan State will have a very low debt to GDP and investors would love to invest in it”.

A very low debt to GDP does not mean anything. Brazil has 56% and is junk status.Andorra has a 41% debt to GDP and issues very small amounts above the EU rate, and is two points from junk. The Baltic countries had no access to markets after independence despite their low debt. The debt to GDP is one of several elements to analyse risk. That is stock of debt. We must analyze the repayment capacity.

The repayment capacity is clouded by the uncertainty of the whole process. In the absence of certainty about the impact on economic activity, tax revenue, capital outflows, etc, no one takes an optimistic or neutral scenario from the beginning. We must assess the pessimist. All secessions in modern economic history have seen a very significant fall in GDP , and with luck, a recovery in the medium term in V shape. And overwhelmingly, it has happened in countries rich in commodities and that brutally devalued the currency. Pensions and social spending in real terms suffer as the economy stabilizes.

“… Fiscal balances are enormous”.

Fiscal balances are not a cash concept. On day one of the Catalonia independence it does not count with 9 billion euro of added revenues, starting from the fact that the much-discussed figure is only an estimate. Not least because the tax revenue estimate includes those of Catalan companies paid to the central government as income tax and “owed investments”, all that before thinking of “Inversion Deals” (Catalan companies establishing headquarters elsewhere to avoid the impact of secession). In the best of cases, without counting the costs of the independence of 4.5 billion euros, Catalonia would have a deficit of 10% between revenues and income. The transition cost figure is calculated by the National Transition Council.

Even the National Transition Council acknowledges that the Catalan state must be financed through patriotic bonds and “bonds tradeable for future taxes”.

Welcome to the underlying risk. A bond whose underlying is supported by unknown and future income when there is no clear and predictable regulatory and tax framework. And whose principal is not guaranteed if those revenues don´t appear!

“… But the Catalans banks are covered by the ECB”.

Suppose it,s true -and it is more than likely that they would have to move headquarters to access the ECB, which in any case would mean another loss of tax revenue to Catalonia-. The bonds issued by the “new State”, if placed, would not have the support of the ECB and would not be part of the repurchase program (QE). Therefore, in the banks’ balance sheet these bonds would be high risk and without warranty of the central state or the ECB, the risk premium would, at least, be very high. And the amounts raised would be very small to non-existent for years, as has been seen in all similar cases. In all.

No wonder the Catalan bond yields have soared 40% in a matter of weeks.

“… But they will have to accept it”.

Okay, Mr. Lacalle, all this may be true, but as Catalonia is a very important economy, the EU, rating agencies, investors and the world will have to bow to whatever we want, whenever we want. Oh dear, just what Tsipras and Varoufakis said about Greece, which resulted in the success we all know.

General election risks

Spain has showed an impressive recovery. Leading employment creation in the EU, 3.2% expected GDP growth, strong PMIs and growing consumption and confidence.

However, the risk of a coalition between the Socialist party and Podemos is not small, because it will be predicated on undoing the structural reforms that have made the country lift itself from recession, introduce more rigidity in the labour market and intervention in the economy, as well as increase spending when Spain is still far away from complying with the 3% deficit target.

The impact of unwinding the reforms has been measured at 1.5% of GDP, but it could be much larger if the foreign investments that the Spanish economy so badly needs, simply stop.

Coalitions spell trouble for the economy. As I said on CNBC “they won’t agree on anything, and that will stop reforms from being passed”.

At this point, all the parties are promising higher spending. Higher public spending runs the risk of a higher deficit, which analysts caution could trump a recovery.

“It’s a lethal combination, increasing public spending and increasing taxes. Because what happens historically [in Spain] is that they spend more than what they bring in from taxes … revenue from taxes don’t cover the increase in spending so the deficit widens,”

Raising taxes, increasing public sector spending, adding intervention and rigidity is what made the country spend more years in recession than most comparable economies. It destroyed 3.5 million jobs while doubling public debt to “invest in growth”.

Spain will not get the unemployment rates of the UK or the US copying the Greek or French interventionist model. When you copy the policies of stagnant economies, you get the growth of stagnant economies.

Analyzing the risks is not to scare. It is being prudent. Ignoring the risks and assuming a happy land of superpower funding is simply suicidal.