“The real goal should be reduced government spending, rather than balanced budgets achieved by ever rising tax rates to cover ever rising spending”. Thomas Sowell

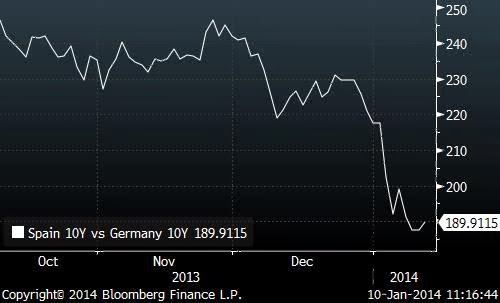

Spanish bond yields have fallen to pre-crisis levels despite debt to GDP reaching c100%, a deficit that will be above the target 6.5% and refinancing needs of c€224bn in 2014. The “Draghi put”, added to much better comps on unemployment (fallen by 147k in 2013), consumer spending (+2% in December) and added to expectations of an 0.5%-1% growth in GDP have helped.

But challenges remain. Debt (public and private above 300% of GDP), unemployment (26%) are still too high, and 0.5-1% growth is simply not enough.

- Spanish banks’ dependence on the ECB will fall from the €220.5bn of November but is still very high. In that month the Spanish Banks long-term ECB borrowings dropped by €12.0bn.

- Bank Non-Performing Loan Ratio. This ratio likely continued to rise in November (from 13.0% in October). In the next few months, the NPL ratio should continue to rise, although at a slower pace.

- Taxes: 40 tax raises between 2011 and 2014. And raised again in the beginning of 2014 to try to collect one billion euro more, increasing Social Security contributions as well, affecting mostly SMEs and self-employed.

Prime Minister Rajoy will be in Washington (13 and 14-January). On Monday he will meet with Christiane Lagarde just a few days before the IMF releases the update of its 2014 growth forecast. The IMF could raise its forecast for Spain from the current +0.2%. On Tuesday, he will meet with the US Chamber of Commerce.

I read different analysis of Spain’s growth potential. Among all OECD countries, Spain is the only one that shows more divergence between expected growth (+0.5-1%) and its potential (+3% according to BBVA, Goldman Sachs and Merill Lynch). This is the opportunity cost of holding on to the 2004 model of state intervention and bureaucracy.

I estimate Spain’s growth for 2014 at 1% and assume 250k net job creation, but this is far away from its potential. Only by laying out the red carpet to job creation and improving the opportunities to do business, Spain would attract direct financial investments of 50 billion euro and would create much more new net jobs.

At the peak of the real estate bubble Spain never collected more than 412 billion euro of tax revenues. However, it spends above 70 billion euro more than this historical high tax receipts of 2007, which will never return. A minimum of 30 billion euro per annum of higher expenses than bubble-peak revenues even if we deduct aid to banks and one-offs.

According to the 2014 Budget data Spain will be spending 10 billion euro in subsidies; 23 billion in “coordination and finance relationships with territorial authorities”; 690 million in State foreign action; 497 million in development cooperation; 131 million in “cultural diffusion abroad”; in “peripheral State administration” 275 million; in “news coverage” 55 million; another 83 million in meteorology (yes, I swear); actions “to prevent climate change” another 42 million; official cars spend raises 1.6% to 240 million; the mutual healthcare, which is parallel to public healthcare, means another 2 billion. Yet we hear that there is no scope for further cuts.But the problem is that we don’t give solutions for the two problems which are obstructing the economic recovery:

- A “Sheriff’s of Nottingham” taxation system that is more worried about collecting the last coin and sustaining, at all cost, the unsustainable spending, instead of creating good conditions for economic growth and with them generate more tax revenues. When I read “reform” to “increase tax bases” “reduce deductions” it really means “raise taxes”. Spain is the country where fiscal pressure has increased more since 1965 after Turkey. Fiscal pressure at 40% ranks among the highest in the EU (read here)

- Legal uncertainty perception. If the tax and legal environment are not clear and predictable it will be very hard to attract financial investment to create jobs and put capital in the economy for the long-term. Not to buy bonds and shares, but investing in sectors capable of making Spain recover real growth. If the system is seen ad unpredictable and risks of retroactive changes, long term investment doesn’t arrive. Spain lost ten positions in the ranking of “doing business” of the Heritage Foundation (46 from 36 before).- Useless spend sustains a level of bureaucracy whose objective is to justify itself with endless rules (state, region, local) and ridiculous procedures. I recommend you to read the “additional competences” given to the regional authorities or the unproductive subsidies, for example. This bureaucracy and complexity acts as a block to new investment and job creation. Between 2008 and 2011 public spending in the Eurozone increased almost 7% to nearly 4.65€ billion. In southern countries, the most affected by the so-called “austerity”, at least in theory, the evolution is similar: From 2008 public spending has grown 8.6% in France, 4% in Spain, 3% in Italy and 7.8% in Portugal.