The ECB is creating a dangerous bubble and should not have cut rates by 10bps nor added a new purchase program of €20 billion per month.

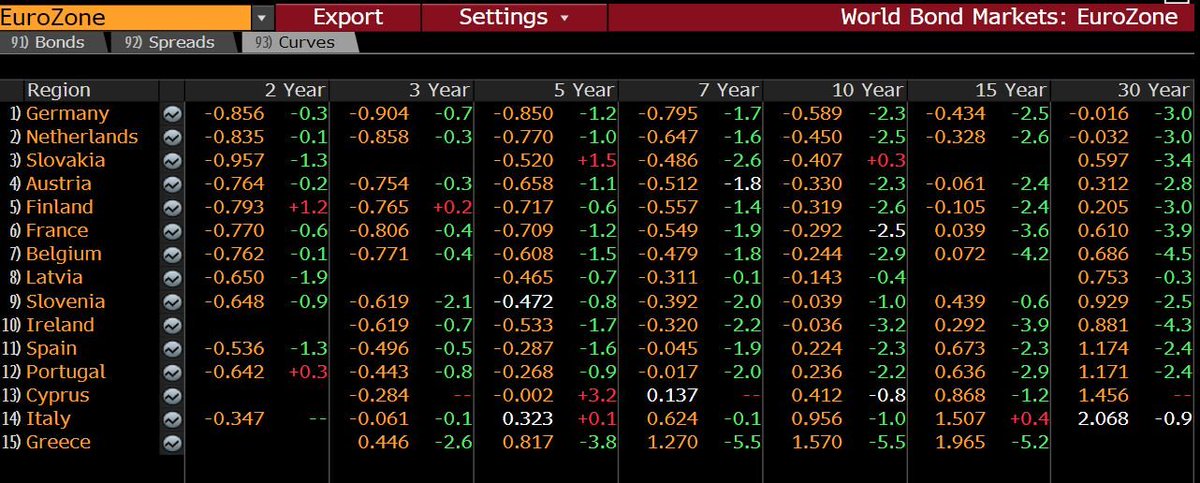

1) Eurozone states are already financing themselves at negative rates. There is no need for lower rates and this disguises real risk.

This has saved governments more than 1 trillion euro in interest expenses (handelsblatt.com/today/finance/…)

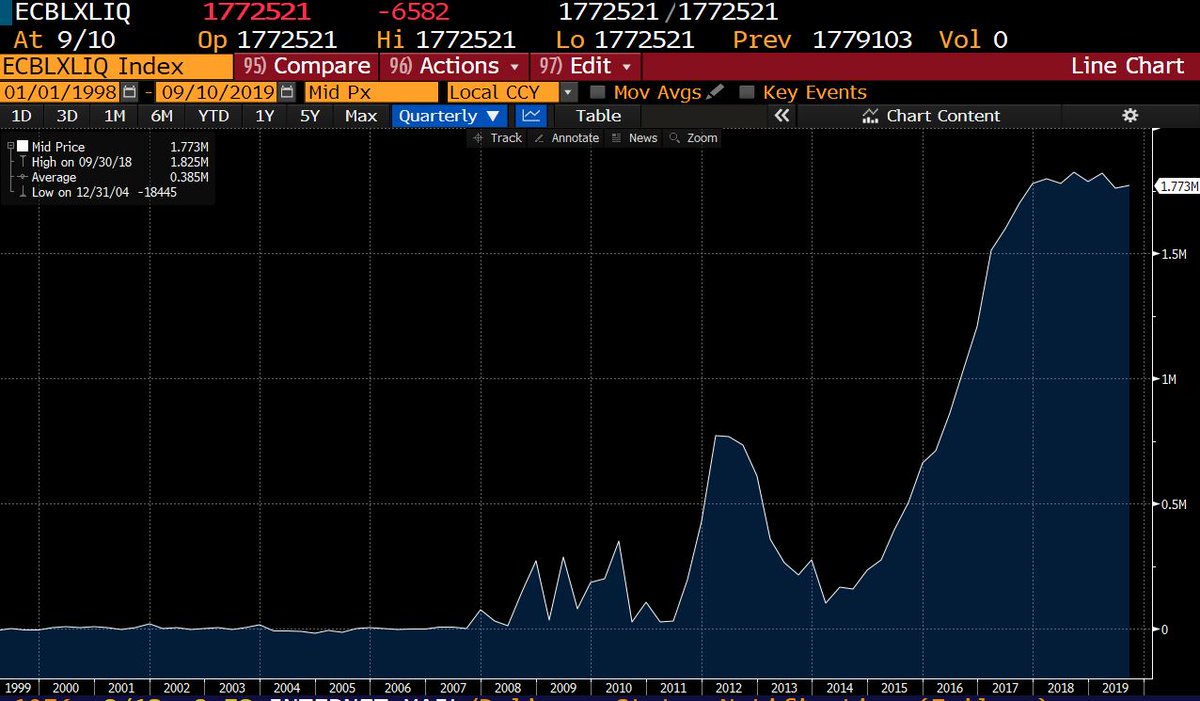

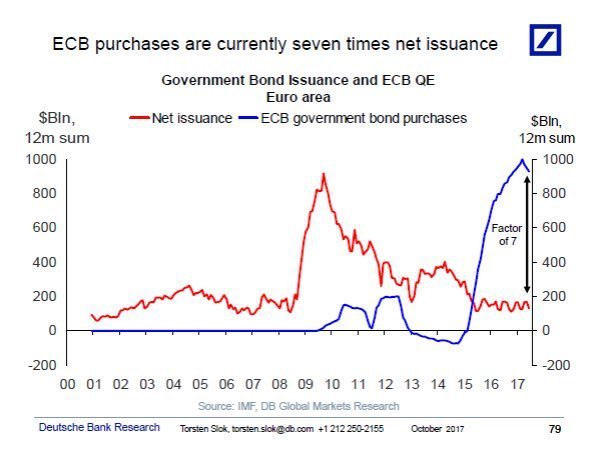

3) Excess liquidity is 1.7 trillion euro. More liquidity does not lead agents to spend/invest more.

There is no higher solvent credit demand because monetary policy perpetuates overcapacity and zombifies the economy. Share of zombie companies has soared c30% since 2013 (BIS)

The ECB believes the eurozone problem is one of excess saving and lack of demand when it is of excess debt and oversupply.

This disguises risk and creates an enormous bubble.

This disguises risk and creates an enormous bubble.

8) The problem of the eurozone is not one of lack of stimuli, but an excess of them.

Governments burden the productive private sector with higher taxes and unnecessary regulations, so economic surprise falls despite massive stimulus.

10) Saying that negative rates are “demanded” by investors is a sad excuse.

Financial repression leads economic agents to take more risk for lower yields and central banks go from lenders of last resort to enablers of financial bubbles.

Spot on analysis, it will all end in tears worse than 2007/8 2&2 are 4 not five