Senator Elizabeth Warren recently stated that rising prices were due to corporations increasing their profits. “This isn’t about inflation, this is about price gouging for these guys”. It is simply incorrect.

No, corporations have not doubled their profits, and rising prices are not due to the evil doings of businesses. If evil corporations are to blame for rising prices in 2021, as Elizabeth Warren says, I imagine that they were magnanimous and generous corporations when there was low or no inflation, right?

Inflation is the tax of the poor. It destroys the purchasing power of wages and engulfs the little savings that workers accumulate. The rich can protect themselves by investing in real assets, real estate and financial, the poor cannot.

Inflation is not a coincidence, it is a policy.

The middle class and the salaried workers not only do not see the advantages of inflation, but they also lose in real wages and also in their future prospects. Robert J. Barro’s study in more than 100 countries shows that an average 10% increase in inflation during one year reduces growth by 0.2-0.3% and investment from 0.4% to 0.6 % in the next year. The problem is that the damage is entrenched. Even if the impact on GDP is apparently small, the negative effect on both growth and investment remains for several years.

Despite the message from central banks, which repeat that inflation has temporary components and is fundamentally transitory, we cannot forget:

Inflation will not go down in 2022 according to central banks, inflation will go up less in 2022 than in 2021. It is not the same.

When some agents speak of “transitory” inflation, they mean that it will rise less in 2022 than in 2021, not that prices will fall.

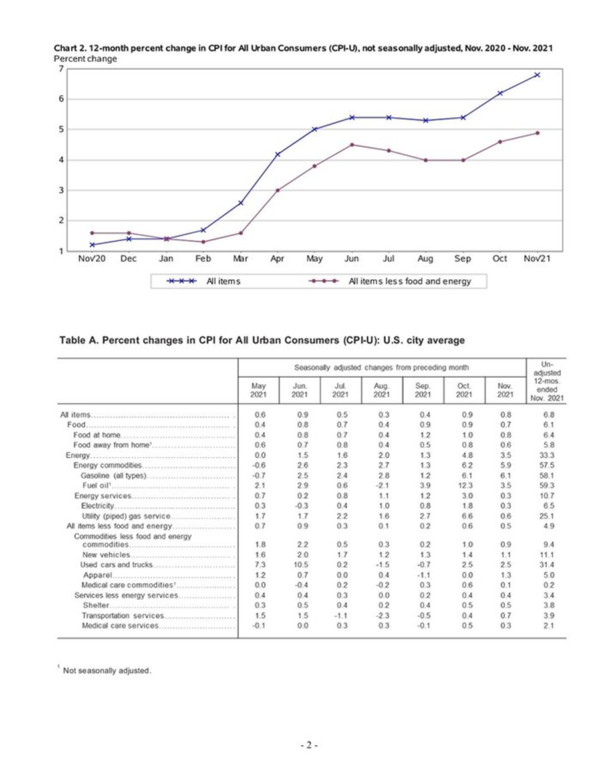

“Transitory inflation” is 6% in 2021, 3% in 2022 and 2.5% in 2023. That is, more than a 12% increase in three years. How many of you are going to see their wages and earnings rise 12% in three years?

The great beneficiary of inflation is the Government, and Ms Warren knows it, that is why she defends inflationary monetary and fiscal policies. On the one hand, receipts from the monetary taxes of captive economic agents increases (VAT, personal income tax, corporate, indirect taxes) and on the other hand the government’s accumulated debt is partially ‘devalued’. But public accounts do not improve because GDP slows down, the structural deficit remains high and, therefore, absolute debt does not fall.

How many of you are going to raise their salary 12% in three years?

Deficit-spending governments see real expenditures go up and the structural deficit does not fall.

Wages and pensions do not rise with inflation. Almost no one will see a 12% rise in three years in their work compensation. Real median wages in the United States have plummeted due to inflation, according to St Louis Fed data.

Inflation is not the CPI (consumer price index). Inflation is the loss of purchasing power of the currency that leads to a persistent rise in most prices regardless of their sector, demand, supply or nature, and is a direct consequence of the wrongly-called expansionary monetary policy. Inflation is a direct cause of currency debasement.

CPI is a basic basket calculated with estimated weights between goods and services. In it there are prices of non-replicable basic products that rise much more than the average and that we consume every day (food, energy) and the basket is moderated with services and goods that we do not consume every day (technology, leisure,…).

Prices do not rise in tandem at a 2% to 5% because of a coordinated decision from all businesses in all sectors. It is a monetary phenomenon.

The good thing for the most interventionist politician is that the Government is the most benefited by the rise in prices but it can blame others and, on top of that, present itself as a solution by giving a payment in increasingly-useless paper currency.

The history of monetary interventionism is always the same:

- Say that a nonexistent “risk of deflation” must be fought: Print.

- Say that there is no inflation even if risky assets, real estate and the prices of non-replicable goods rise more than the CPI. Print more.

- Say that inflation is due to the base effect. Print more.

- Say that inflation is transitory. Print more.

- Blame businesses and companies. Print more.

- Blame consumers for “hoarding”. Print more.

- Crisis

- Repeat.

The monetary factor is key to understanding the continued rise in almost all prices at the same time. An enormous monetary stimulus destined in its entirety to massive current spending plans, infrastructure, construction and remodeling, energy-intensive sectors, and checks to families financed with debt monetized by the central banks.

To this we must add the effect of the shutdown of a just-in-time economy during the pandemic, which generates some bottlenecks exacerbated by massive money supply growth.

Much of what they sell us as “supply chain disruption” or input cost effects is nothing more than more money directed at relatively scarce assets. More amount of currency directed to the same number of goods.

Professor John B. Hearn explains it: “Stephanie Kelton, a prominent advocate of MMT, stated that “all inflations for the last 100 years are cost push inflations” Both MMT and Keynesians require an explanation of inflation, for their theories to progress, that can explain how inflation occurs when there is deficient aggregate demand in the economy. As much as we want to believe that oil prices, energy prices, wage rises and falling currency values can cause inflation it is just not logical. By definition all inflations are defined by more units of money used in the same number of transactions. All of the above can change relative prices, but none of them can increase the number of units of money in the economy. There is therefore only one cause of inflation and that is the action of a Central Bank who, in a modern economy, manage the stock and flow of money in that economy”.

Indeed, a good or service can rise in price due to a temporary effect, but not a generalized increase in the vast majority of prices. When they try to convince us that inflation does not have a monetary cause, they make us look at a good or service that has risen, for example, by 50% temporarily, but they hide us that the median of essential goods and services rises more than the CPI every year. That is why Keynesian economists always talk about the annual CPI and not the accumulated one. Can you imagine if you read that inflation in the eurozone at the time we were told that ‘there is no inflation’ was 45%?

Professor Batten in an article published by the St. Louis Federal Reserve explains: “The cost-push argument views inflation as the result of continually rising costs of production — costs that rise

unilaterally, independent of market forces. Such an hypothesis (1) confuses changes in relative prices with inflation, a continuously rising overall level of prices, and (2) neglects the role that the money supply plays in the determination of the overall price level. The idea that greedy businesses and/or labor unions can cause a continual rise in prices cannot be supported by either the conceptual development or the empirical evidence provided. Alternatively, the hypothesis that inflation is caused by excessive money growth is well supported”.

Why was there no inflation a few years ago?

First, there was. Massive inflation in risky assets, but also constant inflation in real estate prices, costs of essential and non-replicable goods and services. And a large number of countries in the world have been suffering inflation due to the destruction of the purchasing power of the currency in that period we were told there was “no inflation”.

Second, the increase in money supply in the eurozone or the United States was less than the demand for credit and currency in aggregate terms since they are global reserve currencies with global demand. Although the money supply increased a lot, it did not translate immediately into prices domestically. Excess of money supply remained in the financial system, thanks to the inflationary brake mechanism that quantitative easing has, which is the real demand for credit.

Inflation has been unleashed when the credit demand brake mechanism has been partially eliminated, directing new money supply to direct current spending by governments and financing subsidies to economic agents in the midst of a forced shutdown of the economy. Supply of money supply far exceeds demand for the first time in years.

According to Morgan Stanley, the biggest impact on companies is the collapse in margins of those who cannot pass the increase in costs to their prices and this especially affects SMEs, while large companies can manage inflation better, but profits do not double… In fact, margins tend to fall.

There is a paradox whereby many businesses see their sales rise but their margins and profits fall. That is why bankruptcies and foreclosures have skyrocketed.

The impact of inflation is especially negative on the most disadvantaged citizens, who have a basket where energy and food weigh much more.

The UN food price index has soared to a decade-high and is up 47% since June 2020, while natural gas is up 300%, oil 60%. Industrial businesses also suffer margin declines with aluminum rising 36% and copper 20% in 2021.

The problem is that this situation can generate a significant problem for the vast majority of the population. That is why it is so urgent that central banks stop the monetary madness and normalize monetary policy. If the monetary excess is maintained with the excuse of “transitory inflation “we will find ourselves with a problem that took many decades to control: persistent inflation and the risk of stagflation (inflation with economic stagnation).

Those of us who work in the financial sector cannot fall into the perverse incentive of defending inflationism just to scratch another rise in risky assets. Our obligation is to defend monetary sanity and economic progress, not to encourage bubbles. Let’s attack inflationism before it attacks us all.

Really Daniel, one of your best. This has logically increased my awareness of the financial straits we find ourselves in. Thanks for creating something easy to read and understand.

You cannot tolerate being proven wrong, which is all the time.

Your comment is hilarious, ludicrous

How about commercial banks which lend money they don’t have by simply “writing in” a credit into the borrower’s account? What effect does this almost universal practice by most commercial banks have on inflation?

Commercial banks may cause monetary inflation only if and when the central bank incentivices it through rate and money supply policies.

Being an underdeveloping country, causes of inflation in Pakistan are due to twin deficits,

1-Fiscal deficit and current account deficit

2- since export prices are not priced sensitive as a result of which depreciating currency value does not increase its exports but further increases inflation. As currency depreciation makes imports costlier.

3- there is no indirect relationship between inflation and employment.

4- Due to IMF conditionalities, growth gets slower and slower, which leads to a vicious cycle of underdevelopment. Low Income, Low savings, Low Investment, and again low income.

This is a dilemma in nutshell about inflation and economic growth of Pakistan