- A hippie is someone who looks like Tarzan, walks like Jane, and smells like Cheetah

- I’ve noticed that everybody that is for abortion has already been born

- Here’s my strategy on the Cold War: We win, they lose

- Socialism only works in two places: Heaven where they don’t need it and hell where they already have it.

- The nine most dangerous words in the English language are: “I’m from the government and I’m here to help.”

- The government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.

- How do you tell a communist? Well, it’s someone who reads Marx and Lenin. And how do you tell an anti-Communist? It’s someone who understands Marx and Lenin.

- It has been said that politics is the second oldest profession. I have learned that it bears a striking resemblance to the first.

- I have left orders to be awakened at any time in case of national emergency, even if I’m in a cabinet meeting.

- Recession is when your neighbour loses his job. Depression is when you lose yours. And recovery is when Jimmy Carter loses his.

Category Archives: Sin categoría

Top 10 Gene Simmons quotes

Top 10 Gene Simmons quotes:

- Life is too short to have anything but delusional notions about yourself.

- “Men want success and sex. Women want everything.”

- In America you are given the opportunity to be whatever you want to be. The rest is up to you.

- Walk amongst the natives by day, but in your heart be Superman.

- Whoever said `Money can`t buy you love or joy` obviously was not making enough money.

- My hero is me. Why? Because I was the kid who was told, `Hey stupid, can`t you speak English?` Now all those people work for me.

- You can’t argue with facts and figures. Either people want it, in which case they pay for it, or it`s two guys at the Plaza having a discussion, which means nothing.

- The root of all evil isn`t money; rather, it`s not having enough money.

- “When you walk through a bad neighbourhood, you don`t want a poodle by your side. You want a Rottweiler.” On why he voted for Bush

- Anyone who tells you they got into rock n` roll for reasons other than girls, fame and money is full of sh*t.

Spain’s 2013 Budget Needs Red Pencil Slash

This article was published in El Confidencial on Sept 29th 2012

“Deficits mean future tax increases, and politicians who create deficits are tax hikers”, Ron Paul

Spanish 10 year bond yields remain stubbornly at 5.85% while spreads widened to 450 basis points after the announcement of a budget that provides more questions than answers.This week El Confidencial published that the Spanish Government restated the 2011 budget deficit from 8.6% to 9.44% and 2012 could slip to 7.4% from the current 6.3% target. We talk constantly of regaining market confidence, but such confidence is not going to come with constant budget revisions. It will be achieved with better than expected numbers. This is the reason why I am concerned about optimistic assumptions in the budget and aggressive tax increases added to generosity in maintaining a bloated state. I mentioned a few months ago that Spain needs to apply the red pencil throughout a bloated state that spends, even in alleged “austerity times” the same funds as in the peak of the housing bubble (see here).

Spain will have to borrow around 200bn euro in 2013. That is 567 million euro per day.

The 2013 Budget is a step, but an insufficient one

Spain’s Economy Minister, Mr Montoro, said that “it is impossible that Spain has lost 70 billion euro in revenues only due to the crisis.” With the number of companies in business falling from 155,000 to 135,000, the real estate bubble bursting from 650,000 homes built per year to 150,000, the collapse of the industrial activity of 2% per annum and the rise in unemployment to 24%, I think it is admirable that revenues have only fallen by 70 bn euro.

While economic measures focus in recovering lost revenues of the housing bubble that will not return, the investor perceives that Spain could forget about the medium-term risks of a predatory fiscal policy.

Voracity in tax collection with possible impact in the medium term

Almost half of the budget adjustment is, again, tax increases that reduce consumption,weaken the economy and prevent companies from creating jobs.

In a recent analysis, JP Morgan warned about a few key aspects: loss of deposits, industrial decline, poor profit margins and stagflation. The loss of deposits is less than what is estimated in the press, announcing almost 120 billion, but we should never underestimate 30 billion as “irrelevant”.

However, in Spain between 1500-2000 companies file for bankruptcy each quarter. In addition, the CPI soars to 3.5% when GDP decreases 1%. This risk of “stagflation” -inflation with recession- can be very dangerous for the economy. All this happens in an environment where profit margins have decreased to make many of the large companies and SMEs generate margins below cost of capital. The economy remains extremely rigid and tax increases are reflected in the prices immediately. Adding an unemployment rate of 24% to the equation creates a difficult horizon for recovery.

While the general government deficit remains a concern, we must also highlight the positive , and in July there was a current account surplus of 500 million euro. This is important because, if confirmed as sustainable, it implies that Spain reduces its external financial dependence .

We must appreciate it, but we must not forget that it is, in part, the result of the inability to continue to import due to falling industrial demand. Spain is still not competitive and structural reforms must stem the drain on companies, rigidity and erosion of profit margins inflicted by aggressive tax increases.

If companies are not created, if SMEs do not generate profits, then banks do not finance, debt increases, tax revenues collapse … and deteriorated companies do not hire…and the unemployed do not consume.

If we prevent businesses and citizens from becoming richer, we impoverish the country

Goldman Sachs called the 2013 budget “Running to Stand Still” referring to the U2 song about drug addiction. The market is concerned about optimistic tax revenue expectations (+4.4%) and estimates of increase in social security contributions that are inconsistent with the government’s own estimates of unemployment increase. The market sees a high risk of seeing expenses rise above estimates and revenues fall short of target.

For example, sensitivity to two items is enormous. If VAT revenues do not increase by 13%, as budgeted, and they will very likely not increase due to loss of consumption, then the government’s estimates of tax revenue growth would fall to almost zero.

If transfers to regional governments continue in 2013, something which is quite likely given the regions’ troubled situation, that means another 12 to 16 billion of additional spending.

In terms of budget targets, it appears that the government has fallen into the same trap of previous governments. To provide estimates of GDP growth (-0.5%) that few analysts consider as conservative. The consensus range for 2013 is between -1.2% and -2%. Should the government not have taken the opportunity to build trust giving estimates in line with the consensus of economists and then beat expectations? Beating estimates is essential to regain market confidence.

The goal should be maximum expenditure, not “deficit as a percentage of GDP”

To avoid suspicions on revenue estimates, the state should give a maximum target of spending and put up remedial measures every time such goal was surpassed. If the target is “deficit to GDP”, it masks poor budget execution with ratios that can be manipulated.

Austerity? Where?

What I think is most important to note is that these budgets, as those of 2012, cannot be described as austere. Public spending rises by 5.6%. Yet I hear over and over that the problem is “the cost of debt” … as if the cost of debt was an alien who came down in a UFO surprising the population. As if such cost of debt is not the result of massive public spending.

But even if we deduct the cost of debt, primary expenditure falls only by 0.6%. This is before the regional communities publish their expenses and before any deviation due to bank bailouts or “unexpected” one-offs.

This is not austerity, it is, at best, a slight budgetary restraint

I do not know of any family that comments about their budget “we are doing okay if we remove the cost of the mortgage.” The Spanish budget does not show real cuts, just very slight revisions of previous years’ overspending.

We should highlight it because there is a huge difference between austerity and “less overspend”. Spain will keep spending, including all administrations, almost 20% more than it earns, and will also spend more than it earns without the cost of debt, leading to having to borrow around 200bn a year.

The difference between the “red pencil” and the “Troika axe”

As Art Laffer said, “give me a red pencil and the budget and I will reduce the deficit to zero in a week”. The reduction of debt, not the deficit, is the only solution. And that will come only from cutting spending. Or the Troika will do it for us, but they will do it unfairly and badly.

It is important to repeat that the State and the regions should reduce absolute expenses much more severely, that the state cannot be 56% of the economy, including all public enterprises and that Spain cannot spend 20-25% more than it collects as revenues.

There must be serious cuts in political spending. The presidents of regional governments or ministers cannot have more counsellors-each-than David Cameron.

The Spanish fiscal consolidation process will not be credible unless it structurally reduces the largest expenditure items.

The red pencil. The State can immediately attack four items:

- Public salaries , a spending of over 100 billion. We have higher public wage expense per GDP than the EU average but a number of civil servants per citizen that is less than the EU average (Eurostat). What is the problem? Too many bosses and too little workers.

- Consultants and duplicated administrations, which, according to the Association of Businessmen and the PP when it was in opposition, cost more than 22 billion euros. Even if it was half it would be too much.

- Unproductive investments : In the central government budget of 2012, direct investment in infrastructure- useless high speed trains, ghost “culture and arts” cities and others- amount to 11 billion. According to the latest Stability Program, the gross fixed capital formation, which includes more than infrastructure, was 2.8% of GDP in 2011, and another 1.0 to 1.2% is expected in 2012 and 2013.

- Subsidies: The amount in 2011 was 11.3 billion and, even in 2012 and 2013, subsidies are expected to exceed 0.8% of GDP. If we add transfers and ministries, we easily reach 15 billion.

Of course, dozens of public television networks, hundreds of public radios… If we attack subsidies and administrative duplication Spain can avoid the “axe” that will come with the bailout, which will look at the expenditure items of over 30 billion and sever them, no matter who is affected and how. Those who call for an immediate bailout request tend to forget what comes with it:

- Pensions, a cost of over 100 billion. They may have very significant cuts.

- Unemployment benefits, which generate a cost of c30 billion.

- Dismissal of civil servants. Not pay cuts, dismissals.

The impact on companies

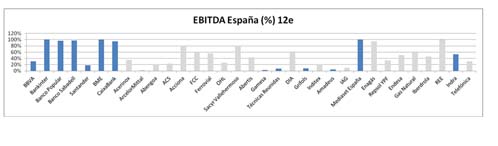

The Spanish budget impact on companies is not irrelevant. In a very interesting analysis, Ahorro Corporacion shows the companies that are most exposed to Spain (in blue) and exposed to civil works, capital-intensive activities (in gray).

The impact of the Budget, if we assume that the fall in GDP is only 1%, ranges between 5 and 7% of net profits. Less revenue from income tax, less growth, fewer jobs.

These budgets should have aimed at reducing Spain bond yields. They didn’t.

We know that the country risk will not be reduced if revenue estimates are revised down, spending items are revised up, and debt accumulates with a state structure that survives with short term emergency loans from the ECB without any control of how and when they are granted. Spain runs the risk that the system is not only tax-ridden and confiscatory, but insolvent … and investors, financial or industrial, might think that such risk is too high to invest.

From Bloomberg:

As per the Ministry’s budget statement, Spain plans to borrow €207.2bn next year. Budget Minister Cristobal Montoro said Spain’s debt will widen to 90.5% of GDP in 2013 as the state absorbs the cost of bailing out its banks, the power system, and euro-region partners Greece, Ireland, and Portugal. He added Spain’s budget deficit target of 6.3% will be met because it can exclude the cost of the bank rescue. This year’s budget deficit will be 7.4% of economic output.

Further read:

Market implications of a delayed bailout

This article was published in El Confidencial on Sept 24, 2012

“Spain’s meltdown is so huge that Al Gore would make a documentary about it”

Last week, I was fortunate to meet with many Spanish companies. Their transparency and prudence is what helps us to improve the country’s image with investors despite the erosion of results from tax greed, political noise and anti-foreign harangues.For investors, it is not easy to position themselves ahead of the last quarter. On one hand, we see the stock market go up and the Spanish risk premium holding the 400 basis point level, even if it is at levels that were considered intolerable a year ago. And Spanish companies have taken advantage of a window of credit that opened in September to go to markets and refinance part of their debt.

In fact the week from 10 to 17 September, according to Goldman Sachs, was the busiest week of corporate bond issuances since 2009, at almost €21bn. But unfortunately this is not enough, and companies have issued bonds for one third of their needs for the next twelve months.

What does the debt market tell us? Public or private debt?

The good news is that Spanish companies can access capital market and are doing it at spreads that are not very different from what we saw in 2008-2009, about 300 basis points above the benchmark (midswaps), with demand exceeding supply by four times.

What the bond market tells us is that there is appetite for debt of companies as long as it’s well secured by assets. That appetite should be exploited.

It also tells us that the debt market has no appetite for sovereign debt. When the government published the July budget execution, most economists had already written off the deficit target of 6.3 percent in 2012. In June, the deficit of public administrations was 8.56 percent. Regardless of all the taxes and cuts that they want to announce, it is virtually impossible to reach the budget target, which has already been revised upwards three times, as shown in this chart of JB Capital.

Thursday’s auction was extremely revealing. Weak foreign demand is concentrated in the short term -three years- which is where the European Central Bank would supposedly buy and therefore only a few hedge funds are betting on an imminent intervention. The long-term tranche -10 years- was disappointing, only €901m, showing the lack of international demand.

This is one of the most important things that I always explain to my readers when I read that Spain “has no public debt problem” but a private debt problem. Yeah right … Spain doesn’t have a problem because there is no demand. No demand, no problem. With public debt at historic highs, €804.4bn and 75.9 percent of gross domestic product, which is in reality 110 percent of GDP if we include all the concepts, we’re headed to have one Exxon plus one Apple in debt. There is no bigger problem than to have financing needs of tens of billions annually and have no institutional demand. Just like a store without customers.

a) Private debt, no matter how weak companies are, is secured by assets that can be sold more or less expensive, but are sellable. Public debt is just spending, it disappears, it generates no return and is used to maintain duplicate administrations, loss making public enterprises like Omnium orInvercaria, and to bail out the public saving banks… Yes, all public. To all those that demand a nationalized banking system, congratulations, this is the result.

b) Private companies can raise capital and sell assets. The state either curtails spending or raises taxes and cuts services.

c) Private debt default risk is almost 40 percent lower than that of public debt because confidence in managers is significantly higher than in politicians.

d) Half of Spain’s private debt is concentrated in 30 companies. Not one of them has losses and negative free cash flow that match the disaster of our public accounts. The state loses €45.2bn in six months. The state spends nearly double its income. Find me a single large company or SME that spends twice its revenues. Not remotely. And do not tell me stories that the state has a social duty. The first social duty is not to spend money they do not have, and not to sink future generations speculating that everything will go up.

Therefore, we have a budget implementation which does not induce optimism.

– Very few investors believe that tax revenues will grow by 17.9 percent between 2011 and 2014, because we are living the Laffer curve in all its glory. More taxes, less income. And in this item rests nothing less than 28 percent of the estimated improvement of national public accounts.

– Very few investors believe Spain will reduce spending watching the evolution of expenditures so far. In fact, many investors believe €20-30bn more will be needed to cover the hole of the savings banks in 2013, and many fear that the government’s objective is to maintain GDP at all costs, even keeping unproductive expenditures.

Investors resoundingly favour corporate bonds and continue to avoid a sovereign bond that is only discounting the option of a bailout. Government debt held by foreign investors has continued to fall while Spanish banks have offset this decline.

What if the bailout is delayed?

The delay makes sense, but the bailout is inevitable:

– As I mentioned in this column, once the bailout is requested, the country runs the risk of being labelled as junk status. While a rating agency says it is not going to do it, the market will likely do it. It is of paramount importance to give companies the ability to finance all they can and to raise capital before Spain is treated as junk bond.

– The conditions can be very aggressive and with the liquidity and solvency indicators of European Union countries worsening, Spain runs the risk of making a bad deal. Spain will have to make huge cuts anyway, and everyone wants to give the impression of calm and prudence.

– Perceived political problems. Elections are close and no one dares to appear in front of voters saying “ladies and gentlemen, what we have to do is to apply the red pencil.” I’m surprised, because people know and all they ask is that someday the red pencil is applied to official cars or the hundreds of politicians paid by taxpayers’ money.

What we do with the IBEX at 8230?

“Bull markets are born on pessimism, grown on skepticism, mature on optimism and die on euphoria” Sir John Templeton

We have gone from the “worst is over” to “the best is yet to come” and the risks of complacency abound.

We will end September and Spain is the only European country that bans short positions. And now the government calls for a tax on short term gains. Against speculators, they say. Of course, to them selling a stock is speculating, but building statues and unnecessary airports is “investing.”

McCoy in El Confidencial wrote an article mentioning that the IBEX could be a great investment opportunity based on CAPE (cycle adjusted price to earnings). However, I have doubts. How can we value today’s companies using the last cycle when the past meant massive debt, huge subsidies and real estate bubble growth?

My opinion is:- The IBEX is not cheap. The consensus expects earnings growth in 2013 of… 52 percent. I swear. Normalizing these estimates, the Ibex at 12xPE and 3.8 percent yield is not cheap, except for three sectors, industrial, and electrical consumption. Look at this chart by Mirabaud.

– Once we establish that the IBEX cannot give big surprises in its expected profits, the surprise can only come from the average weighted cost of capital (WACC). It has improved thanks to the cost of debt, but the cost of equity is rising and the impact on stocks will be dictated by their ability to continue refinancing themselves cheaply … and by country risk. If the market puts Spain in junk bond, the brutal positive impact generated in August can be reversed.

– The IBEX remains the most indebted index in Europe, which is why it goes higher when liquidity injections are discounted and falls more when financing is a risk. The refinancing needs of companies can lead to a situation that we call “cannibalism,” that is, the bond supply offsets the interest in shares when marginal investor appetite focuses exclusively on corporate bonds, not stocks, as we saw in 2008.

Spain will have to make real cuts, not tax increases. We cannot see the bailout as a solution and forget the risks for companies. I hope our dear politicians, who complain so much about speculators, will stop speculating with the money of others betting that in two years all will go up, because they are turning Spain into the worst hedge fund in the world.