BBC World Service. Listen to the interview in the link here.

What the Trump administration was doing was a negotiation tactic. Aggressive, bulldozer-type and, of course, questionable. But a tactic to address the massive trade deficit with China, the largest in the world, at $375 billion. The negotiation tactic is clear, as proven by the tariff moratorium on the European Union, Canada, Mexico and South Korea.

China needs the U.S. surplus more than the U.S. needs China’s trade and finances. And that is why the trade war will not happen. Because China has already lost it.

This is a duel at dawn in which it is most likely that no one will shoot … Because the pistols are loaded with debt, not with gunpowder.

The trade war will not happen for various reasons:

China badly needs the surplus with the United States to keep its extremely indebted growth model, way more than the United States needs China’s purchases of debt of goods. China added more debt in the first quarter of 2018 than the U.S., Japan and the EU combined, and it has reached an estimated 257% of GDP. If it does not grow exports to its main customer, the U.S., its problem of overcapacity and debt soars, and the economy crumbles.

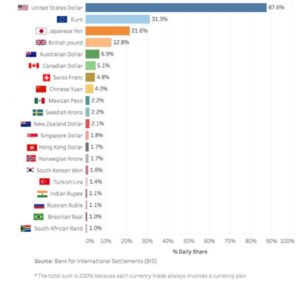

- China cannot win a trade war with high debt, capital controls and US exports’ dependence. A massive Yuan devaluation and domino defaults would cripple the economy. The U.S. dollar is the most traded currency in the world, and growing according to the Bank of International Settlement. The Yuan is 4% of currency trade.

China’s currency is not backed by either global use nor gold. At all. It is as unsupported as any fiat currency, like the U.S. dollar, but much less traded and used as a store of value. China’s gold reserves are an insignificant fraction of its money supply. Its biggest weakness comes from capital controls and intervention. However, even with capital controls, capital flight has continued. $51bn outflows in the first quarter of 2018, according to Natixis.

China’s currency is not backed by either global use nor gold. At all. It is as unsupported as any fiat currency, like the U.S. dollar, but much less traded and used as a store of value. China’s gold reserves are an insignificant fraction of its money supply. Its biggest weakness comes from capital controls and intervention. However, even with capital controls, capital flight has continued. $51bn outflows in the first quarter of 2018, according to Natixis.- China does not have a nuclear option on the U.S. debt. For once, it is not the main owner of U.S, bonds, not even close (China is less than 8.6% of U.S. bonds outstanding). The United States can guarantee the demand for its debt issues even if China sells. But, in addition, China has increased its purchase of U.S. bonds by $168 billion dollars since the U.S. elections. If China sells its Treasury holdings, its own currency would massively appreciate and the domestic risks, lower exports, lower growth, outweigh the threat. Even if it sold, the demand for U.S. bonds has increased and when China has reduced Treasury holdings, Treasury yields have fallen. The Federal Reserve and the main U.S. Fixed Income funds could buy the bonds in a very short period of time, a week at most. Remember that 2018 has seen a record pace of inflows to U.S. Treasuries. $3.4 billion inflows in one week, with year-to-date inflows of $18.6 billion (data April 14th, 2018).

- China cannot maintain its growth – based on a huge debt bubble – if its exports fall. And its trade surplus with the United States has been growing while its trade surplus with the rest of the world shrunk. A drop in the growth of China’s exports would mean a collapse of foreign currency reserves. These reserves have been recovering a bit recently, but have fallen 21% since the 2014 highs.

A collapse in the reserves of foreign currency would accentuate the capital flight that is already taking place, which would lead to increasing the already disastrous capital controls in China, and with it, three effects. Lower growth, higher debt and the risk of a very important devaluation of the yuan.

For China, a trade war would be devastating.

Of course, there are important negatives for the U.S. but not as dramatic.

The United States exports very little (12% of GDP), so any threat that leads to a positive agreement is an exponential improvement. But the duel is loaded with wet gunpowder.