This article was published in El Confidencial on Sept 19th, 2012

“Paper money eventually returns to its intrinsic value – zero.” Voltaire Continue reading The Myths of Paper Money

This article was published in El Confidencial on Sept 19th, 2012

“Paper money eventually returns to its intrinsic value – zero.” Voltaire Continue reading The Myths of Paper Money

This article was published in El Confidencial on September 8th 2012

“In central banking, as in diplomacy, style, conservative tailoring and an easy association with the affluent count greatly and results far much less” John Kenneth Galbraith

Euphoria. All is solved. After Thursday’s announcement from the ECB regarding unlimited purchases of short-term sovereign bonds, Draghi and Merkel, the “enemies of Spain and Europe,” according to some press, are now our saviours. Investors seek to protect themselves against inflation through stocks and commodities. By now there is no doubt that we are moving towards an inflationary period driven by financial repression and aggressive monetary policies.

From my point of view, the ECB plan only manipulates the price of short-term bonds artificially. Access to ECB funding is not linked to growth and solvency and is not aimed at rewarding the efficient. It will provide liquidity judging only by price without questioning whether such price is fair or not. It also runs the risk that countries receiving the liquidity will delay reforms knowing that if they push the limits they will receive a bailout. In essence, the ECB could be breaking the principle of responsible lending, a mistake that, in my view, is affecting the entire EU and discouraging long-term investment and capital.

I also believe that this plan simply transfers peripheral risk to countries like France, which do not have sufficient economic strength to endure the added risk. But above all, the ECB plan leaves the medium to long term solution of the economies in pro-state policies that do not promote the creation of new businesses and jobs. In the US I hear talks of SMEs, private job creation and growth, while in Europe it seems we only read about more government debt, to maintain subsidies and how to protect an unsustainable state apparatus, which acts as a crowding-out predator of credit to companies and families.

Questionable premise

The first mistake the ECB plan has, in my opinion, is to think that the bond yields of peripheral countries are “unfairly high”. It happened before with Greece and Portugal. It starts from the premise that bond yields are higher only because of the “fear of a euro breakup” when the reason is pure and simple of solvency. The problem would be much easier to solve if Spanish bonds were discounting an “imaginary” exit from the euro, but what we are seeing discounted is a much more problematic issue. Spain spends twice its revenues.

The negative surprises such as upward revisions in the deficit of Valencia by €3bn –a tiny 82% “mistake”-, the Catalonia bailout, the savings banks’ bailouts, a state deficit that has already reached 4.6% of GDP and that, including regions, may well be significantly ahead of the government target for 2012 … All these issues make the market discount that the gap between expenditure and revenues will expand further because costs do not go down. If the market believed that Spain runs the risk of leaving the euro, bond yields would stand well above 6% due to the inability of the country to finance the primary deficit outside the Eurozone.

The risk of perverse incentives

I see the 10-year bond at 5.6% and I fear that politicians will dust-off the cheque-book for more unneeded infrastructure and construction projects. Savings banks are denying credit of tens of thousands of small and medium enterprises –which generate 80% of added value and 70% of jobs in Spain- yet they seem more than willing to provide lending to high risk construction projects promoted by the regions and financed mostly with debt.

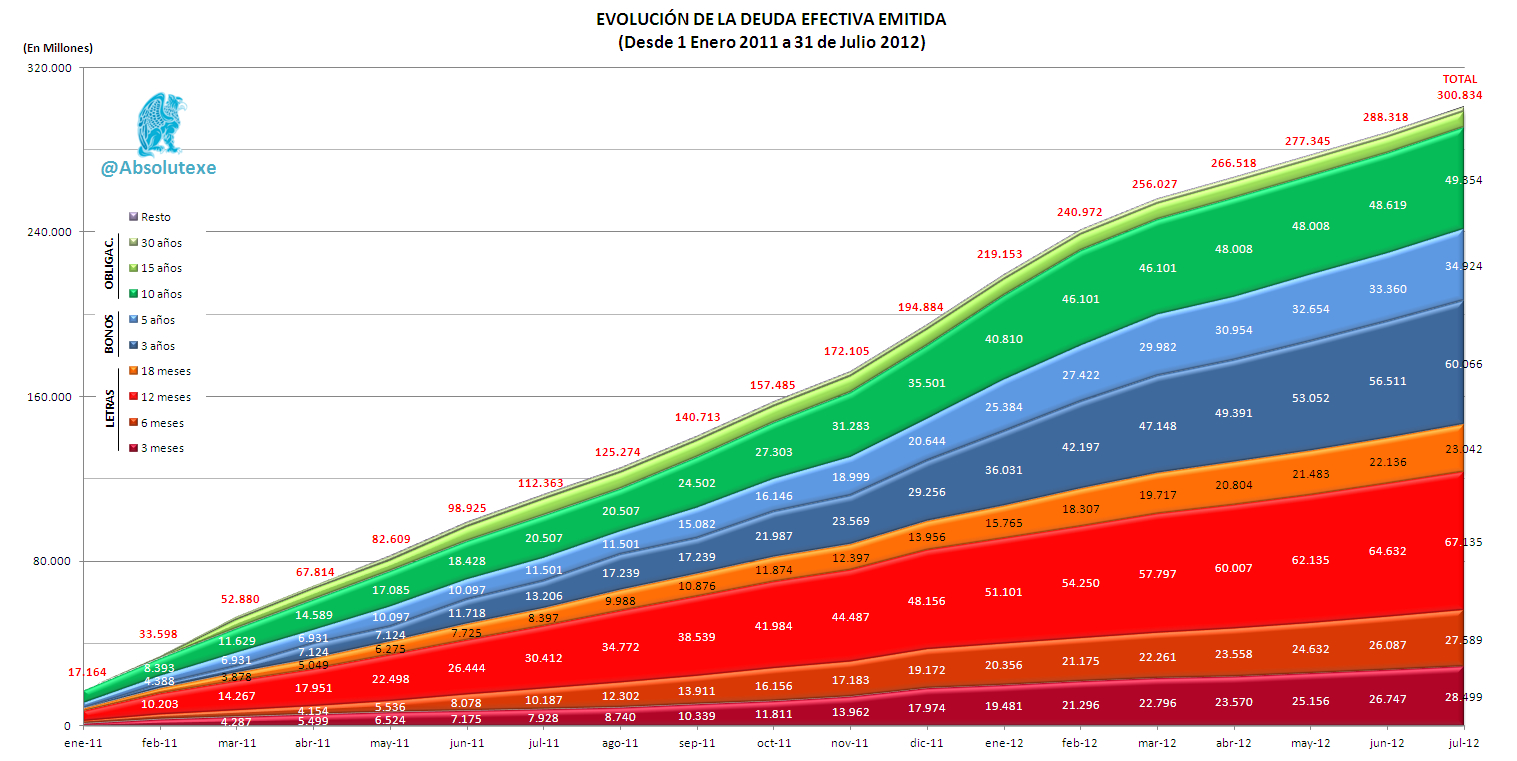

The most dangerous incentive generated by the ECB plan is that countries with greater difficulties will concentrate most of their debt in short-term bonds, which is the tranche that the ECB would buy, because they know that the long-term maturities will have very little institutional demand. The ECB expects that by doing so it will “force” investors to buy long dated debt. I believe the ECB is wrong. Think of the example of a company with poor fundamentals that sees one of its controlling shareholders buy more shares “to support the stock”. Investors do not follow this move except for the very short term. The monetary regulator assumes that credit investors “must buy” European debt and expects that by announcing “unlimited purchases” it will create a steady demand. In my opinion, this is incorrect as the underlying problems of the economies of peripheral countries are not even close to be solved, and will likely be postponed and dragged once bond yields are “perceived” low enough to “spend again”.

I am concerned about countries which are concentrating too much short-term debt, as the chart shows. The risk is multiplied because they are funding unproductive state spending and long term government investments with short-dated bonds, a dangerous recipe.

We must also note the danger of having “cheap” credit, which could lead many governments to delay cuts and, taking advantage of the complexity of the administration, take another spending party before the Troika comes and citizens see another round of tax increases.

The words that scare me: “unlimited capital”, “strict conditionality” and “sterilization”

The really sad part of the ‘rescue’ plan of the ECB is that not a single cent of that money goes to small and medium businesses, to create jobs. It goes to support a hypertrophied structure of the state, which will continue monopolizing the available credit under the promise that “something” will fall for the real economy … And it does not, because added to this ECB support countries face the urgent need to recapitalize banks, deleveraging. That is, less credit to households and businesses.Instead of supporting banks and government apparatus, and hoping that some crumbs will remain for the real economy, imagine what it would be if families and businesses were the recipients of this “unlimited capital”. Crisis over.Strict conditionality. The carrot and stick. Another problem is that the ECB plan makes countries very dependent on the ECB buying bonds to fund them while the European regulator threatens to withdraw such support if conditions are not met. The countries will be at the mercy of a quarterly ECB revision of its accounts and, therefore, subject to much greater volatility.

The strict conditionality also implies that budget cuts will be very severe. But because those cuts should be reflected in the accounts urgently to continue accessing the ECB line, governments might not focus on long-term structural reforms, focusing instead on elements of immediate impact. Tax increases.

Unlimited capital.

The ECB has not yet bought a single bond and euphoria takes over markets based on a word: “unlimited”.

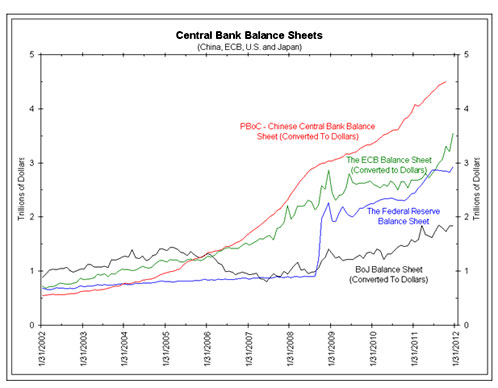

I’m surprised to hear those words as if they were logical. Unlimited capital. The Eurozone GDP fell by 0.4%, more than 2000 companies file for bankruptcy each quarter, unemployment keeps rising and Europe sees plummeting fiscal revenues. But we read “unlimited” without printing money. Unlimited means generosity with other people’s money. It means debt, and lots of it in a European Central Bank whose balance sheet in 2012 is close to 34% of Eurozone GDP, close to 3 trillion dollars, much more than the Fed (20%) and the Bank of England (21%) in their countries.

Sterilization means that for every bond it buys the ECB has to sell other assets to prevent inflation from rising out of control and to avoid borrowing massively. Sounds good? But so far Europe has proved unable to contain inflation, just disguise it, and the ECB debt has soared by 20% annually.The issue is that the central bank will be manipulating prices but will not increase liquidity in the system. Why do it then? It only impacts prices short term but the debt and liquidity crisis lingers.Another problem is called France, which would see bond yields soar just as it is growing debt and credit ratings will suffer, as Moody’s has warned. If added to this the ECB also sells French bonds, it will weaken another engine of Europe.From the point of view of institutional demand, foreign capital is likely to continue to avoid Europe as ECB intervention becomes a constant stream of “plugging holes” changing the price of assets and then, investors simply will not be able to invest in European debt on fears that prices are manipulated randomly and according to subjective criteria.

Reforms are not debatable

Every newspaper in Spain demands a bailout as if it was a donation and the end of budget cuts. It is neither. The ECB does not donate, it lends. Spain would not need a bailout if it managed expenses according to revenues, rather than waiting for the return of fiscal revenues of the housing bubble period to finance a hypertrophied state. And the consequences of a bailout are very relevant.

A bailout has a huge impact on the creditworthiness of Spain. And even if rating agencies will promise no downgrade to junk status, the market will do it, as it did with Portugal, Greece and Ireland. Spain has to assess this risk.

Minister De Guindos said Spain is carrying out the reforms that Germany undertook 10 years ago. Let us hope it is correct.

It is easy to reject reforms from Spain’s current perspective of a heavily subsidised nation with an “undeniable right” to debt, and claim that cuts don’t work. To illustrate why reforms are essential I would like to end with a few sentences of an article about Germany’s 2004 reforms, “The three crises that undermine the European colossus ” written by Jose Comas and published in El País in 2004, when many believed Spain was the rich champion of the world:

“Germany is riddled by corruption, recession and deteriorating public services. Its crisis is structural. Convinced of the need to renew a stagnant Germany, Schröder launched in March of last year the ‘Agenda 2010’ reform program. It was a plan to make cuts in social benefits rooted in post-war German culture, and to partly dismantle the achievements of social capitalism: reducing social benefits in retirement, health care, unemployment and making layoffs easier. Schröder opened the bottle and let go the spirits that will lead to political ruin”.

Schröder must be singing “I Hate to Say I Told You So” by The Hives.

This article was published in El Confidencial on September 1st 2012

“When you blame others, you give up your power to change”

“A sense of entitlement is a cancerous thought process that is void of gratitude and can be deadly to relationships, businesses, and even nations.” Steve Maraboli

On Friday, Standard & Poor’s downgraded the rating of Catalonia to junk after the region made a bailout request to the Spanish central government of €5bn. S&P warned in its report of the “economic and credit deterioration of the region,” and added that “the region’s request to modify key institutional and financial aspects of its relationship with the central government raises uncertainties that we deem incompatible with an investment-grade rating.”

The report also warns that “Catalonia continues to show a poor individual credit profile, with a deteriorating liquidity position dependent on the support of the central government to repay its debt.”

The bailout of Catalonia has generated much controversy in the market, but it’s worth saying that my comments in this article are applicable to most of the regions in Spain.

Despite the huge amount of communication efforts towards investors conducted by the different regions, all with ‘more GDP than Luxembourg and less debt than Japan,’ all considering themselves entitled to borrow indefinitely, the fact is that regions have no access to capital markets. And this shows how, all across Europe, countries and regions continue to believe that credit is free, investor money is unlimited and deserved without questions. And there is no unlimited capital.

The excellent presentation to investors that the Catalan government, theGeneralitat, made in 2011, very complete and detailed, shows some of the common problems that Spain and the regions face, and the reason why investor confidence and interest are still low.

. Estimates that were very optimistic: “Our revenues cannot fall.” “In 2012, with very conservative estimates, revenues will increase by 10.5 percent.”

. A debt maturity schedule that implies annual needs of €3bn added to the current financing needs of nearly €9bn. Added to that, the habit of financing current expenditures with long term debt and weakening future revenues, as Catalonia has received advances on transfers of more than €10bn until June 2012 – advances spent today that will not be collected later.

. The average maturity of the Catalan debt is six years. More than 71 percent of its debt matures between two and five years. I always tell my readers of the importance of not accumulating short-term maturities in good times as risks accelerate exponentially in times of recession. Accumulation of maturities well above marginal institutional demand is a problem throughout the European periphery coming from the misperception that “there is plenty of available demand” in the credit market for all, when the United States and major countries account for nearly all of the debt market capacity.

. Expectations of international funding sources were not met and have only been partially covered by local retail investors.

The real problem, however – the reason why investors do not rush to buy Catalan bonds that give a return of nearly 12 percent in 2016 – is that it has been proven since 2004 that any increase in revenues is engulfed by the regional administration and as such, the risk of default is higher than implied by companies and the region’s financier, the Spanish central government or Germany.

I heard this a few times from colleague credit investors: “a country that doubles its expenses in four years while its revenues fall, either has oil, or gold, or it does not have my money.”

The 10-year-Catalonia bond has a risk premium –spread– to Spain of almost 600 basis points and 1,100 basis points over Germany. This difference is not because of Catalonia’s dependency on Spain, or the alleged fiscal deficit. It is caused by the massive deterioration of expenditure and revenues, and the accumulation of debt maturities far beyond institutional demand. And it is important to say this, Catalonia is one of the regions with better credit structure. So, imagine the rest.

In fact, if investors perceived the massive spread between Spain and Catalan bonds as unjustified by the fundamentals, they would take the arbitrage opportunity and load up in Catalan bonds. Any credit arb hedge fund would buy them in size. But they don’t.

Now the blame game heats up. Spain blames Germany, Catalonia blames Madrid, Andalusia blames the banks, etc. Meanwhile, with on-going downward revisions of the gross domestic product and failures in budget implementation, governments continue to believe in the mantra of eternal credit ‘because we deserve it,’ sinking the ship with the crew and passengers inside.

In the Spanish regions and the central government, each euro received of additional income, either through taxes or transfers and structural funds since 2004, has become inexorably a euro and ten cents of debt. Looking at the Spanish regions, all the money received has been spent, but all of them have expanded primary deficit as well. In 1993, the regions managed 20.1 percent of the country’s budget, today they manage nearly 60 percent, yet all of them spend far beyond their means and income, regardless of their business and economic differences. Here in Spain there is no poor state. No Alabama. We are the United States where everyone is Washington or California.

This leads us to a comment made by my esteemed Xavier Sala i Martin, Spanish-American economist at Columbia University, who says that the problem of access to debt markets for companies is mainly because they are Spanish, and that if Catalonia were an independent country “it would be considered one of the world’s healthiest economies and financial markets would rush to lend it money.”

In this post, I am joined by my fixed income colleague to give readers an idea of how the debt markets work, because it is false that the main indicators to buy bonds are just debt to GDP and deficit, and I remember the comments from one of the British investors when the premier of the Generalitat made the presentation of its bonds in London. “If Catalonia was an independent country it would have the same access to credit as Andorra,” he said.

But even more surprising to me, as an investor in equities and bonds, is to read that “financial markets would rush to lend money” to an independent Catalonia. That is not true, as we have seen from country after country that declared themselves independent, from Yugoslavia to the former Soviet Union. Either they have abundant energy commodities or credit evaporates until they have gained years of experience as independent states. Estonia, the example for independence movements, only saw some modest short-term credit because Germany broke the treaty rules and recognized the country quickly. Even with that, credit was modest and GDP collapsed by 14 percent in 2009 and 9 percent in 2010.

When investing in bonds – debt to GDP, which is an indicator, inflated precisely by government spending and real estate bubbles – is irrelevant. What matters is the institutional credibility, the acceleration of expenditure against income, the quality and predictability of that income, the weight of public spending, monetary stability and the primary deficit or surplus.

We assume that Catalonia has institutional credibility, but:

. An independent Catalonia would be an economy that depends by 57 percent on Spain for its “exports.” In fact, since the trade balance with “non-Spanish” countries is negative (Catalonia imports more than it exports), Catalonia’s exposure to “Spain” would remain the same if not higher, particularly on the risk of the bonds of the alleged independent Catalonia. The cost of belonging to the EU, however, which Catalonia does not pay today as a region, would expand its deficit. Add to this that an independent Catalonia would have to absorb 18 percent of Spain’s national debt on the way out, and Catalonia would have debt to GDP higher than 100 percent. In a Spanish recession, the independent Catalonia bonds would also aggressively discount that same recession.

That’s why, despite the huge attractions and exceptional positive elements of Catalonia – dynamic, open economy – the investors perceive as the biggest problem the structure of a state that swallows any extra income received as it has done since 1996, making the solvency and liquidity ratios very tight, and this will continue to impact their access to credit. In fact, it is precisely the liquidity ratio, even assuming the previously mentioned tax deficits, which scares investors. Because the deterioration of income – with the deindustrialization of the region into more competitive and less bureaucratic countries, like Morocco – is accompanied by expenditures which can only rise, and do not take into account that the economy of Catalonia is very cyclical.

We end with a note on the “negative impact of being Spanish” to finance large companies. Sala i Martin says that ”the reason (for not having access to credit) has nothing to do with the sector in which they operate or the state of their economic health. The reason is simply that they are Spanish companies.”

First, we have seen debt issues, divestitures and hybrid access by several of these companies (Gas Natural, BBVA, Telefonica and other Spanish companies have issued €7.05bn in bonds with over 10 times demand in 2012), and all are trading at less risk of default than Spain or Catalonia. What we have said in this column many times is the real problem. The average debt of the Ibex is very high relative to its peers due to the orgy of strategic acquisitions at crazy multiples, but we have seen companies do an exercise that neither regions nor the central government have done. Prudence. Aggressively reducing costs, cutting unnecessary investments, cutting dividends, funding themselves long term since 2007 to avoid the “credit crunch.” That is, the opposite of what the governments have done. Companies have been preserving cash generation as an essential policy against an uncertain future, both in its core business as in its “growth markets.”

Surprisingly, Sala i Martin takes as an example of the ‘bad influence of the Spanish state’ three companies with almost monopolistic businesses in national services, telephone, natural gas, and construction-concessions. Great companies which have financed their international expansion with a lot of debt that they have been able to accumulate thanks to very high returns generated in Spain, which allowed them to enjoy better growth than their peers in the past, with full access to borrowing that could not have been there without the support of those domestic revenues and without a Spanish government that supported high risk cost strategic adventures.

No company is Spanish only for the good times and not for the bad times. These large companies, which enjoy a very comfortable monopolistic position in our country, do not suffer lack of credit “for being Spanish.” This is like saying that France Telecom, Veolia, EDP, Telecom Italia or Areva suffer lack of access to credit for being French, Portuguese or Italian rather than their strategic mistakes of expansion with debt.

Catalonia is wonderful and deserves all the good things that can happen there and more, and it is worth a bailout, or twenty, if needed. Spain has regions-nations – whatever you want to call them – with wonderful, huge possibilities. The problem was, and remains, having an unsustainable structure of administrations that absorb any extra income they get. Everyone has the right to claim independence for romantic reasons, or whatever, but we cannot say that the markets would be jumping to provide credit. In five years we would see Barcelona wanting to cut ties with Lleida or Madrid with Guadalajara, until the final implosion of a country with a level of public spending crowding out the real economy that looks like Argentina.

In Spain today, there is a golden opportunity to change, and to unite the country in the solution, not separate ourselves in the debacle. But let’s not blame the other. The solution is in our hands.

——

Here is Mr Sala i Martin’s original article and his reply to my post above

On fiscal deficits. here is the contrarian view to Catalonia’s government one.

“If technologies have economic merit, no subsidy is necessary. If they don’t, no subsidy will provide it”. Jerry Taylor.

“Governmental subsidy systems promote inefficiency in production and efficiency in coercion”. M. Rothbard