I have been reading in detail with interest (but not joy) the reports from OPEC, IEA and EIA.

The main argument raised by the bears about these reports has been to highlight the increase in supply estimates month on month, with different degrees of conviction by the three entities.

There are two main observations to make:

- Seems the consensus has stalled on demand around 83-84 million barrels a day. IEA sees demand down 3% year on year. EIA catched up with this figure and OPEC lowers it a bit (still 0.8mbpd above IEA at 84mbpd).

- Supply estimates remain optimistic: Effective spare capacity has contracted slightly to 5.3mbpd (versus 5.5mbpd) for IEA, which is more optimistic about non-OPEC supply than OPEC (which basically sees non-OPEC output down around 200,000 bpd less than the others).

Two interesting things come in the details though. The fact that supply estimates come predominantly from higher natural gas liquids and production of heavier crudes from mature basins (EIA calls for all projects forecasted in 2009 to deliver in line with expectations in 2009, something that has never happened). Additionally heavier oil means more refining costs and lower quantity of output. Heavy Arabian is trading at $54/bbl. While WTI is trading at $58. Crack spreads are at $10.3/bbl ($8.8 in Cushing). Heavy oils and the increasing cost of de-sulphurization are putting part of the floor on oil prices.

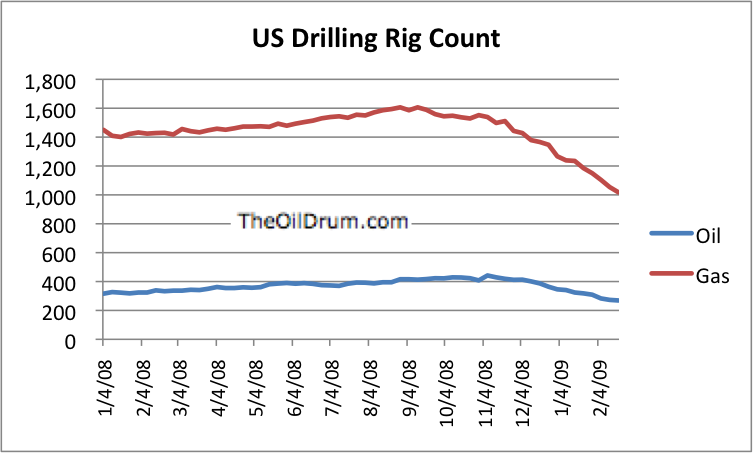

But the interesting point to me comes from what I call the illusion of Natural Gas Liquids (NGLs) which we saw in the past oil “down” cycle (which I painfully lived in the industry). Natural gas liquids are the hydrocarbons in natural gas that are separated from the gas as liquids through the process of (mainly) absorption or condensation. While the EIA, OPEC and EIA estimates continue to put current oil production at around 86m bbl/day, over 10% of this daily production is not oil at all but NGLs. More importantly, all the upward revisions in the three studies about non-OPEC supply come from NGLs. While these liquids are valuable, especially propane and butane, they are not a viable substitute for oil. Fractioning is a highly expensive process and neither can be economically used as a feedstock for gasoline or diesel and cannot be used for current diesel or gasoline engines.

So it is interesting to assess why the estimates are worthy but should be taken with caution. Obviously demand is poor and a clear concern, and while it remains weak it will be a strong driver of oil price movements