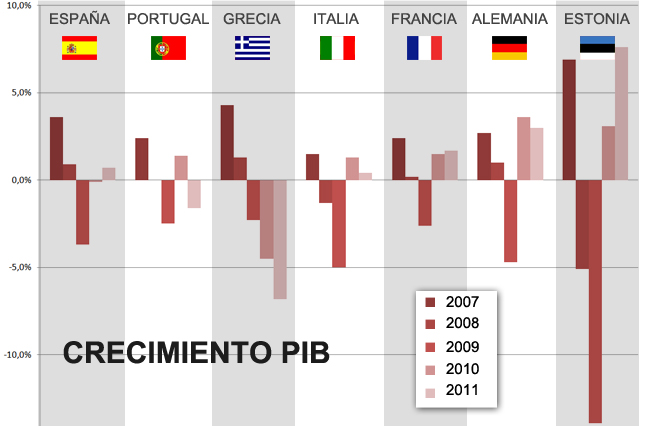

The Greek state, which has more public employees than Spain with four times fewer inhabitants, wasted bailout after bailout and continues delaying reforms, saying that “they’ll come, be patient”. And now, some demand breaking the agreement-yes-after having accepted the money. One thing is to belong to the European club with its obligations and rights, and another is to demand to participate only for the party and not to collect the broken glasses … But it is their sovereign decision to shoot themselves in the foot.To read the arguments in favor of breaking the euro, I recommend the interesting and detailed analysis of Jonathan Tepper here. But I’ll give my opinion focusing on Spain. Leave the euro? No. And I think Spain should not, due to the dangerous implications for the country, its partners and the financial system . Why?

. Because Spain is not rich in oil, gas or natural resources as most countries that have made default and devaluation in the past decades, which allowed them to contain hyperinflation.

. Because even if Spain leaves the euro and enters into a default, it will not be freed to carry out the reforms, adjustments and severe cuts needed due to its structural primary deficit.

. Because Spain can ease its debt problem with reforms and budget control, continuing as a major country in the OECD without breaking the rules.

Leaving the euro, and re-structuring -default, bankruptcy, it’s all the same- to start again is like cheating at cards to try to continue in the casino without paying the debts, and as such you get thrown out. It would lead to a collapse of of 25-40% of GDP quite likely, according to UBS, with 45% unemployment, and hyperinflation.. and then, hopefully, grow.

The examples of devaluation and default in Spain are not encouraging.

Spain devalued the peseta seven times between 1959 and 1993. Inflation and unemployment overshot but what is most important is that by the end of the devaluation frenzy the economy was not stronger, unemployment remained stubbornly high and real inflation -not official- rose well above the expected targets. In the early 90s the so-called “devalue for growth” measures delivered no strong growth and just the obliteration of the middle class for years until the country recovered in 96, mostly due to a massive real estate bubble. Spain devalued in 1992 twice its currency by 6% and 5% and in 1993 by 8%. Unemployment reached 24% (3.5 million), public debt to GDP shot to 68% and public deficit soared to 7% of GDP.

To grow after the shock departure of the euro would require capital. Who would lend or invest in Spain after a blow of such caliber? Just look at the list of countries that have abandoned the reference currencies. Either rich in natural resources or examples of extreme poverty.

In the best case there would be a V effect on growth of GDP. A very doubtful effect that, if anything, would lead to the same starting point. Of the twelve countries that have made mega-devaluations in the last 20 years, none generated a GDP growth remotely similar to the devaluation imposed. Average devaluation of 40% for an average increase in GDP over three years of 10%. Immediate poverty without increasing wealth. As U2 would say, ‘running to stand still’.

An exit of the euro would lead to a devaluation of 35% minimum, default on debt, and the contraction of GDP would be enormous, up to 20% but Spain would continue with a primary deficit problem, which is 3% to 4% currently. The primary deficit is the difference between revenue and expenditure without incorporating the financial burden of public debt.

Spain, as in the bad years pre-euro would have to finance this primary deficit… where? At what cost? In fact, in all cases in the past, the runaway deficit has been the first consequence of the departure of the reference currency . Thus, Spain would have make severe cuts in addition to the drop in investment and disposable income . Leaving the Euro does not free Spain from the much needed cuts and reforms.

At what cost would the Spanish State finance itself outside the euro? The 10 year bond at 6%, which today seems too high, would go to much higher levels. Spain’s financing rate soared to 13% in the devaluation frenzy of the 90s. And CDS in Argentina is 1,196 compared to Spain at 500. And what would happen to corporations? Half of the private debt of the country is held by 28 companies of the Ibex 35 Index. These would bankrupt with the subsequent massive impact on employment.

To think that a Spanish exit of the euro would have no contagion effect in Europe and Latin America, its financial and trading partners, with the subsequent effect on export capacity is also dangerous. Spain would create a domino effect of risk on some European banks, our lenders- as well as defaults on domestic ones, with the consequent spread to Latin America. But once done, Spain would become like Argentina or Ecuador … but without oil and gas, natural resources to keep inflation under control.

Do not forget that Spain is already a net importer of commodities, including agricultural ones. Hyperinflation in such products would lead to extreme poverty, and oe can not be re-orient a nation to autarchy and agriculture in a year.

I remember seeing staff at supermarkets in Argentina changing price tags every half an hour while the government repeated over and over that inflation was just 9%.

Those countries that abandoned reference currencies, made huge devaluations and defaults, kept prices of its domestic oil and gas artificially low to contain hyperinflation. And despite this, inflation shot up to levels of 9% -11%. And in Spain, the “high inflation vs hyperinflation” debate is irrelevant. With 24% unemployment already, 9-10% inflation is hyperinflation.

In Spain, hyperinflation would consume the economy again, as a net importer of raw materials. And the example of other devaluations shows that unemployment is not reduced substantially. Although Argentina doubled its number of civil servants after the de-dollarization, unemployment rose from 14% to to 22% three years later only to fall to an 8% “official” -11% real- rate today, more than 10 years later.

On the other hand, ‘default’ would have a financial domino effect . Given the huge exposure of the banking world to Spain and its private companies, it would create a credit ‘crunch’ at least in Europe if not global. If it happens now with the Greek risk, where we do not know if the impact is 400 billion or a trillion euro, imagine with Spain, which is three times larger than Greece.

But in addition, assuming that the international financial system recovers from the effect of “Spain is out of the euro”, which would take away a good part of the assets of our investors, the country would have very severe financing issues, as it happened in the previous seven devaluations. Because Spain has no natural resources, gold or technology sufficient to make us able to force an autarchy that doesn’t mean “poor for 100 years” . A country back to poor shepherds, farmers and tourism services as in 1960.

Spain is Spain, not Iceland

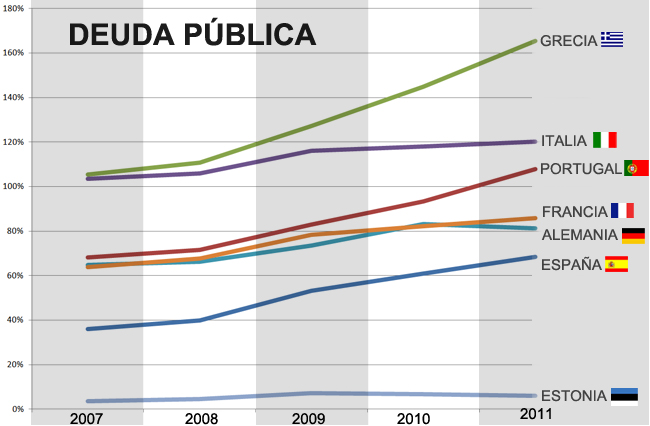

It seems obvious. The bankruptcy of Iceland, a widely used example, was a national agreement of mutual impoverishment in a country of 320,000 inhabitants. Fewer inhabitants than Bilbao. Spain has 47 million. The implications are devastating. Iceland, when broke, was not as relevant for the global economy as Spain is. In 2007, Iceland had a GDP of 8.5 billion compared with a trillion from Spain. The debt of Iceland, at 800% of the GDP was nothing, tiny, in the global financial world. Nevertheless, its default generated a ‘credit crunch’ that affected many countries. The impact of the debt of Spain, which is 3.5 times the GDP of the country is a major risk of an international financial meltdown.

The cost of leaving the Euro of Greece is estimated between 400 billion euros and 1 trillion euros. Spain would be around 2 to 3.5 trillion euros. With that cost, and an impact on financial markets and banks that could last years of provisions and losses, Spain would not see much of a dime of external financing, which would curtail its return-to-growth options.

A problem created in a decade is not solved in one day.

Spain and Europe suffer the hangover from over a decade of debt. And you don’t not cure a hangover from years of alcoholism in two months. Trying quick solutions has a monstrous side effect.

Spain has to lower its debt within the euro, slimming its wasteful spending (14 billion in subsidies, 100bn in duplicated political spending) to improve its creditworthiness and, therefore, make debt less expensive, while reducing total debt. Attract investors and make State with lower and more sustainable costs. Additionally, it must reorient its production model to high-productivity sectors, making an attractive environment for investors, for the entrepreneur. Not all civil works, infrastructure, useless subsidies and housing.

Devaluations and defaults destroy long-term capital investment because it becomes well known that the country will make more and more devaluations, as we did in the past, and defaults.

Spain needs a process of deleveraging in the private and public sector, which, on the other hand, the country can afford without breaking the rules. Another thing is that until today they have not wanted to do because it was easier to wait until more funds from the EU arrive.

In short, the deleveraging is healthy . Growth will not spectacular, but cleaning unproductive sectors unclogs the fundamental problem, that the country borrows to pay current expenses and interest charges. Spain, if it reduces useless expense and the culture of subsides, can reduce debt with modest growth of a mature economy, but with an affordable and sustainable cost and size, appropriate to the cyclical nature of its production model. Not running to stand still.

To watch my interview on Al Jazeera about the Bankia and Spain (Realplayer Quicktime or Oplayer needed): http://dl.dropbox.com/u/62659029/iv_daniel_lacalle_250512_0.mpg

Further read from Juan Rallo: http://www.iea.org.uk/blog/bringing-back-the-peseta-won%E2%80%99t-solve-spain%E2%80%99s-problems

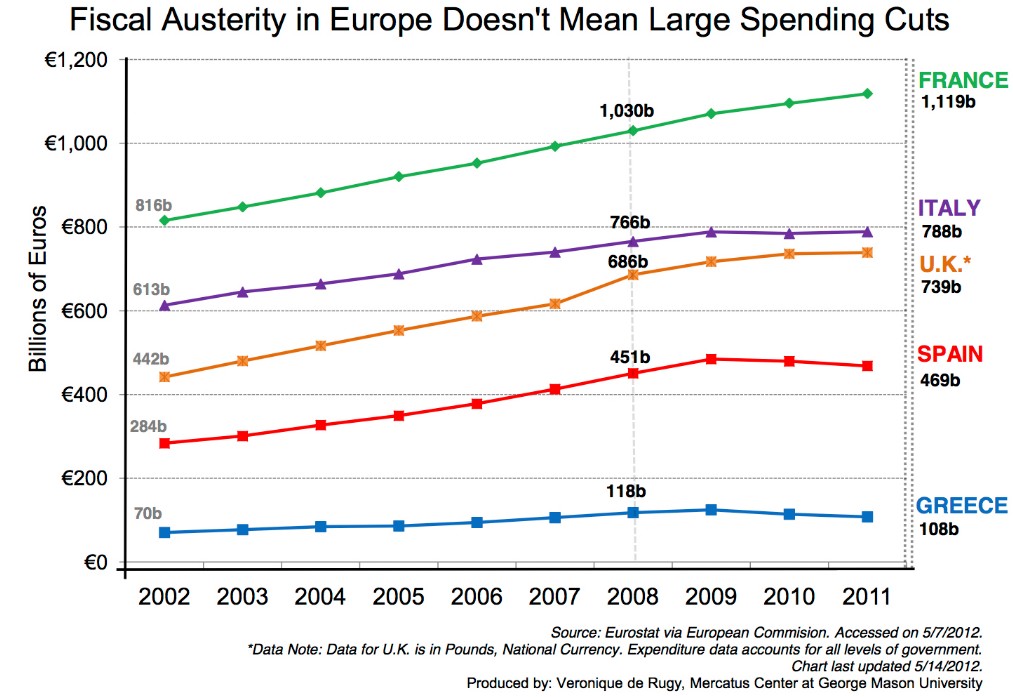

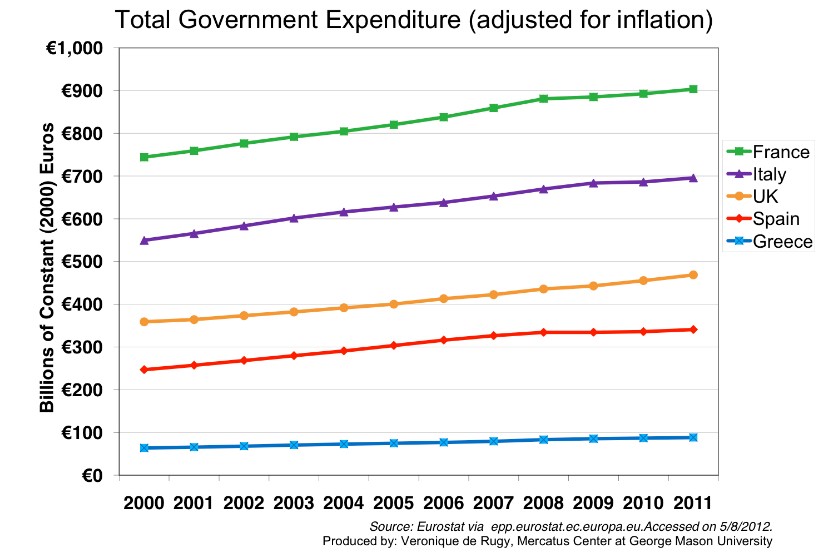

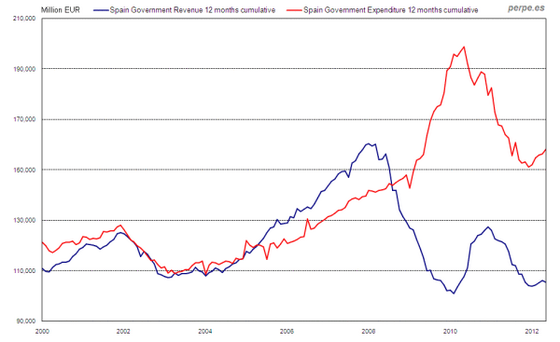

In fact, the situation hardly changed if we look at the evolution of public spending in real terms after inflation.

In fact, the situation hardly changed if we look at the evolution of public spending in real terms after inflation.

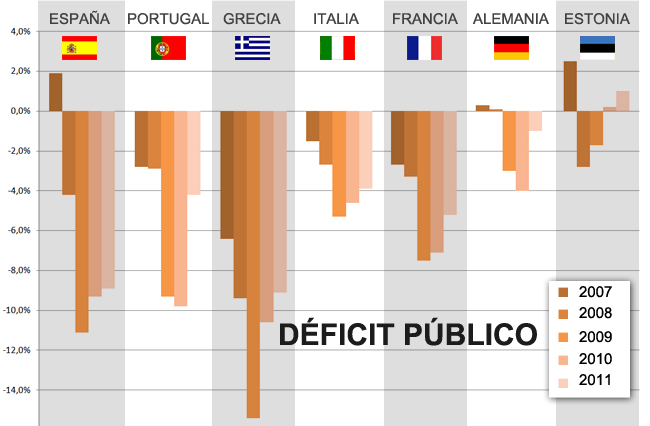

Rescuing Greece does not solve anything in a country that overspends 8% of its entire GDP every year, while revenues collapse and new expenditures appear every quarter. A bottomless pit in a system, the euro, within which it can not and will not recover.

Rescuing Greece does not solve anything in a country that overspends 8% of its entire GDP every year, while revenues collapse and new expenditures appear every quarter. A bottomless pit in a system, the euro, within which it can not and will not recover.