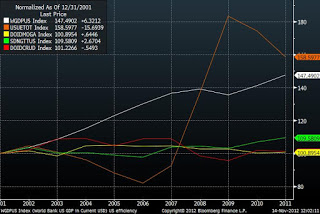

It’s the big news of the week. “The IEA believes that the US will overtake Saudi Arabia in oil output” by 2030.

First, the IEA definition of crude oil is “crude oil including lease condensate”. Does this matter?. To some, yes. Not to me. Differentiating condensate and natural gas liquids from crude reminds me of the debate of oil sands versus API 35 oil. Whatever goes into your tank and makes the car run, baby. EROEI?. Sure, still very strong as shown in my post here (read). My biggest issue is to think EROEI is static and will not improve, when shale gas has gone from 3 to 1 to 6 to 1 in many areas. Continue reading The US path to energy independence in three charts