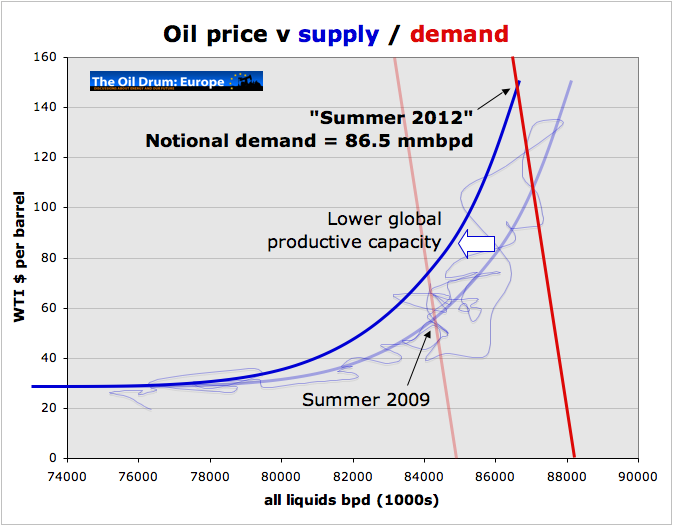

Short term I expect oil to consolidate in these levels, but no fundamental change in global economic outlook to become bearish. Inventories keep drawing, and even with Distillates at uncomfortably high levels, any tick up in demand will quickly absorb excess capacity. Global demand estimates have been revised upwards along with World Bank global GDP estimates for 2010, while capex cuts continue to affect supply, with reserve replacement below 100% since 2004 and decline rates reached 6% in 1H2009. The 10 month contango in oil, with end 2010 at $70/bbl going all the way up to $87/bbl supports this view.

Near-term risk on downside would be if the US$ dollar was to appreciate but financial players are not hugely net long so risk not that substantial.CFTC data shows net long positions in crude at 39,370 contracts, in line with 2006 levels.

Longer-term, downside risk from any reduction in OPEC compliance is offset by likelihood that non-OPEC supplies will disappoint as the year unfolds.Additionally, Iran and Venezuela break-even oil prices are at high end of $50/bbls, so they have a vested interest in keeping compliance to avoid losses.

As for natural gas, the impact of surplus LNG will continue to weigh on the market. LNG’s depressing price impact has been limited (interestingly, YTD LNG volumes are below 2008, so the glut is probably overstated). Meanwhile Continental storage is refilled and pipeline deliveries are moderated. However, by winter the full effect of the surplus is likely to be dragging the 12 month strip down to low 40s p/therm (current 48p/therm).

Oversupplied US gas market likely to keep prices depressed until there are clearer signs of the likely reduction in US domestic production. Medium-term, 12 month strip around $6.5-7.0/mmbtu seems justified (against $6-6.5/mmbtu currently) as domestic production cuts and economic recovery tighten the domestic market, but the oversupplied LNG market restricts any upside.

I expect the effect of the Gas rig count drop to level below 625 and capex cuts in US gas production to show some impact as from September, but even so supply remains more than adequate short-term.

Asian gas prices to remain largely immune from the LNG surplus, and settle at an oil linked $8-9/mmbtu.