Interview at CNBC where I discuss:

The difficulties to implement Quantitative Easing in Europe.

The difficulties to implement Quantitative Easing in Europe come from the increased perception at the ECB and the EBA that a €1 trillion program could distort markets too much as in some cases the ECB would take 100% of supply.

. There is no liquidity issue: To start with, Europe already has more than €180 billion of excess liquidity according to the ECB March report.

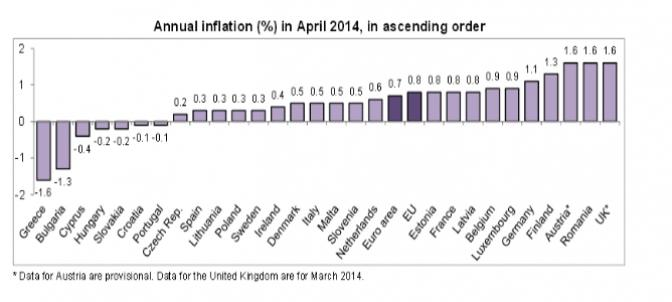

. There is no deflation: Inflation at the Eurozone in April was 0.7% while EU was 0.8%. This is within the ECB mandate of “at or below 2% in the medium term”. CPI in April was 0.4% in Spain, and only Greece (-1.6%) and Bulgaria (-1.3%) show worrying signs.

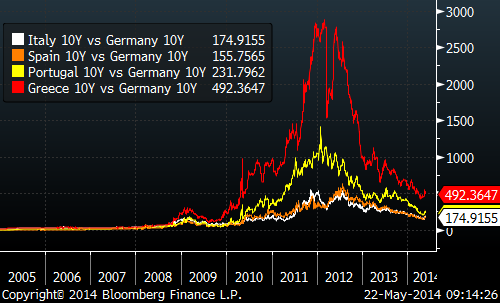

. Bond yields are at historical lows. Bond yields in the periphery have fallen to the lowest level since 2005. Portugal and Greece are out of the bailout program and issuing paper.

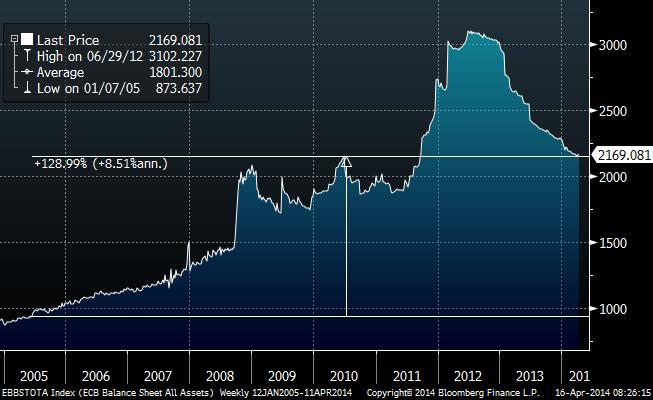

. ECB balance sheet is still elevated. At €2.2 trillion (2.5% capitalization) its balance sheet has fallen 20% since the peak but it’s still up 128% since 2005. The Fed balance sheet is $4.1 trillion (ECB 3.1 trillion translated in US$).

. Transmission mechanism to SMEs is improving. Lending to SMEs is up 34% in the periphery since March 2013.

. Growth is improving (+1.4% in 2014) and the strong euro has not affected dramatically export growth all over the periphery. Current account deficits have arisen in Spain for example. The biggest issue the ECB faces is that 60% of EU exports are made within Eurozone countries, therefore currency is irrelevant. The second is that with current account deficits widening, imports would suffer a big increase in price, particularly energy components. This worries the ECB more than anything else.

However, all of the ECB is studying options of QE driven mostly to help boost the next leg of growth. “Of course any private or public assets that we might buy would have to meet certain quality standards,” said Jens Weidmann, in an interview with MNI.

. What to spend the QE money on?

The European ABS market is too small (€300bn-450bn) for a €1 trillion QE and the challenges would be high when buying sovereign debt in order to adhere to the mandate.

There are three options for the ECB: yield curves, regional differences and credit spreads, which would be targeted in the ECB’s version of unconventional monetary policies. Some of the measures are more akin to Credit Easing (CE) than Quantitative Easing (QE). It is

also apparent that the approach is more qualitative because if the ECB is to make purchases it will take into account valuations.

The ECB would choose from different options, which reflects the bank-based intermediation that dominates in the Eurozone, unlike in the US where the main focus of QE has been Treasuries and MBS. As a possibility, the ECB could choose a normalisation of haircuts on its collateral.

There is also the issue of the “no deflation yet” debate. The Bundesbank is worried about a CPI that reflects massive disparities and that a QE would bring higher inflation to small consumers and average medium income families. The ECB needs more time to see if there is really a price deflation issue. So far data suggests otherwise. No deflation, just disinflation due to overcapacity and previous bubbles.

Look at March CPI in most countries, but particularly in Spain considered at the highest risk of “deflation” by the IMF. Look at essential goods like fish (+3,2%), milk (+4,4%), fruit (+6,5%), legumbres (+3,2%), cheese (+2,2%), natural gas (+2,3%), electricity (+6%) education (+3,5%), insurance (+4,1%) water (+3,3%), or even tobacco (+3,4%), alcohol (+2,4%) or travel (+4,4%).

When you have invested (spent) hundreds of billions of euros in “industrial plans” and productive capacity, especially in energy, car industry, textile, retail and infrastructure, what we are experiencing is a reduction of prices due to competition between oversized sectors, an overcapacity of up to 40% in some cases. On the other hand, inflation exists in other elements, very relevant to the industry and consumption, such as energy costs.

The “alleged risk of deflation” is the excuse of governments to justify greater financial repression . Trying to create false inflation through rate cuts while citizens have less purchasing power, or through monetary stimulus plans when taxes rise leads nowhere. Look at Japan, 17 consecutive months of real wage reductions.

PRICES FALL BECAUSE WE BUILT MASSIVE PRODUCTIVE CAPACITY FOR A DEMAND THAT NEVER ARRIVED AND BECAUSE THE DISPOSABLE INCOME OF CITIZENS HAS BEEN DESTROYED BY CONFISCATORY TAXATION.

To reactivate the economy governments should return money to the pockets of citizens who have stoically accepted and paid interventionist policies and supported schemes and incentives that have led the EU to spend up to 3% of GDP to destroy 4.5 million jobs and sink the economy.

The ECB is getting a lot of pressure to do something from governments and banks, and now even Germany seems to accept the high EUR is a danger… and if something is done it will have to be something big. But these issues above do matter –specially for the Germans advocating for internal devaluation exits to the crisis- and the risks are not small of causing massive distortions in an already booming market for high yield bonds and sovereigns.

See more at: https://www.dlacalle.com/deflation-no-disinflation-the-consequence-of-interventionism/#sthash.Isz8PWji.dpuf

Important Disclaimer: All of Daniel Lacalle’s views expressed in his books and this blog are strictly personal and should not be taken as buy or sell recommendations