(This article was published in Spain in Cotizalia on June 6th 2011)

Seems Germany will approve before mid July 2011 the closure of all nuclear plants (21GW) by 2022 . Adding insult to injury, the country might not remove the tax on nuclear power that utilities already bear.

Meanwhile consumer electricity prices rise as the populations witnesses the effect of their political demands seeing the power bill rise by 45% due to a flurry of subsidies.

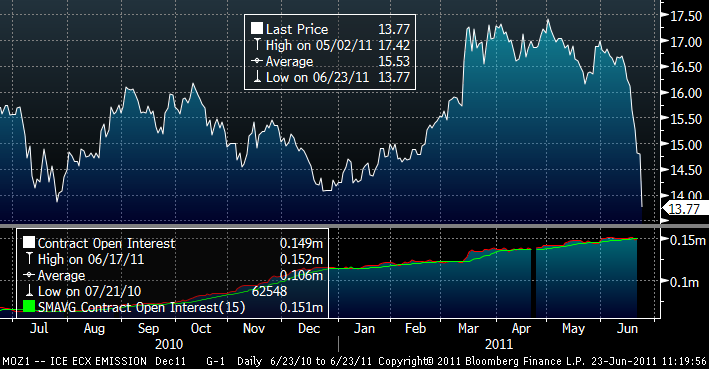

But the move to close the German nuclear plants will also entail a cost of about €40 billion and an additional 45 million tons of CO2 emissions a year (the German government itself expects to offset nuclear loss with lignite coal, gas and renewables). More pollution, but also a cost to the economy of €765 million to buy additional allowances. Of course, the German government says they will implement energy efficiency measures, which have been such a resounding “success” in the past 23 years.

Now Germany will import more power from France, which is generated in its majority with their fifty-eight nuclear reactors.

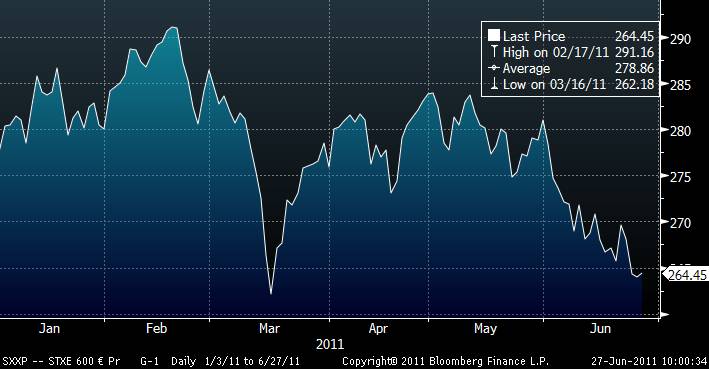

As Europe became more vocal against nuclear power, CO2 emissions increased by 5% in 2010, above the 2008 peak. We pollute more and generate electricity at a higher cost due to subsidies. Not just renewable premiums. Between capacity payments to gas, coal subsidies, market restrictions and other monstrosities, almost all technologies receive some type of subsidy.

Europe, which is less than 30% of global CO2 emissions, runs with 100% of the cost as the rest of the world does not pay for carbon dioxide emissions. Europe embraced the Kyoto Protocol as the ultimate sign of identity of a common political project which did not bear fruit in most other areas, from economy to defence, and is now clinging to its environmental policy, which is the only thing that unites EU countries, at any cost, preferring to pay for all the other countries before reviewing the adequacy of their commitment.

Someone in China or India should be laughing their head off. While these countries continue to grow dramatically, moving ahead with plans to install nuclear reactors (18 in the next ten years), wind, gas, coal and everything needed, Europe becomes the “bill-payer” of Kyoto and shuts down nuclear plants because of the state of fear generated by Fukushima. But who in their right mind expects 9 Richter scale earthquake followed by a Tsunami and a 24 hour blackout in Europe?. (Read more here)

The U.S. has two nuclear reactors under construction, the UAE, China and India have reaffirmed their plans for new facilities, Korea will build five reactors… I’m not saying Europe should build new nuclear plants, first because they are not needed as reserve margins remain high, but those that work should remain active.

The costs for the grid and the system are also important. And no relief for the solar industry. Even if all German nuclear power plants to be closed were replaced by solar power plants the sector would still sell less than half of the solar pannels it has installed in recent years (3.5-4GW p.a versus recent 7-8GW).

For the wind industry, the drastic decision of replacing nuclear also generates a very small positive impact. The global installed capacity has grown from 74GW in 2006 to 200GW in 2010. But the overall installations fell 7% in 2010 and another decline is expected in 2011, just as overcapacity increases. To give you an idea, even using the expectations of the sector, which expects to multiply by three the number of global wind installations by 2020, turbine manufacturers would still have a 20% overcapacity. Also note that in the two main markets for wind, Europe and the U.S. installations have fallen inexorably (50% drop in 2010 in the U.S.) due to the dry-up of public money and the impact of cheap gas (as we said here). In 2012 the U.S. is expected to install 5GW. Annual growth in China, 13-15GW, is constrained by grid bottlenecks.

The only ones benefited so far by the nuclear shut-down in Germany have been the dinosaur gas producers, who were facing a very black-and long-horizon of excess capacity and forced to re-negotiate their long term contracts. Well, surprise, surprise, the gas glut has been half-solved by the anti-nuclear policy.

But it’s no party for gas generators either. Overcapacity in Europe affects the whole energy chain and in natural gas it still exists and it’s quite relevant. The use of combined cycles for electricity generation has fallen to become a mere anecdote that works as “back up” to renewables and European CCGTs continue to generate very poor returns.

The German nuclear power shut-down, therefore, will do nothing but increase the consumer’s electricity bill, and only replaces cheap, base-load power for costly, intermittent peak-load power, but does not solve either the high reserve margins or the efficiency of the system.

Renewables play a very relevant role and will increase significantly in the next five years. But the cost of replacing all nuclear with renewables would be prohibitive and energy dependence would increase due to the lack of domestic natural resources (Germany has lignite, Europe has shale gas, but seems more inclined to ban it than develop it) . Let’s be sensible.

Other related posts:

http://energyandmoney.blogspot.com/2011/03/anti-nuclear-state-of-fear-japan-and.html

http://energyandmoney.blogspot.com/2009/05/reserve-margins-are-clearly-acceptable.html

http://energyandmoney.blogspot.com/2009/10/careful-with-german-power-prices.html